How Much Do I Need to Retire? 5 Different Ways to Work It Out

How much money do you need to retire? There are a lot of ways to answer that question because it depends on your personal situation and circumstances. Also, there are many rules and guidelines that attempt to answer it.

Saving for retirement is important

Saving for retirement may be one of the most important financial decisions you ever make. Get this wrong, and the consequences could be massive. If your guesstimate is too low, you could run out of money in your golden years.

Can you save too much money for retirement? Straight up, my answer would be no, because, have you ever heard someone say, “Gosh, darn it! I saved too much money.”

On the other hand, what if you don’t like your job, but continue working to save, or you lived so frugally, you missed out on the joys of today to save for tomorrow, but when tomorrow comes, you have more than you ever needed.

Here are the most popular rules that answer the question, “How much should I save for retirement?”

1. The rule of 300

This straightforward rule states that you should take your monthly expenses and multiply them by 300. That is how much you need to retire.

So, if your monthly expenses are $5,000, you need $1.5 million saved. The cool thing about the rule of 300 is its simplicity; anyone can figure out their monthly expenses.

Basing retirement needs off expenses, rather than income, is a pretty good idea. It’s also important to factor in those once-in-a-while expenses that come up occasionally, like household repairs or vacations.

Figure out a way to break these down to a monthly amount, because you don’t want to come up short in retirement.

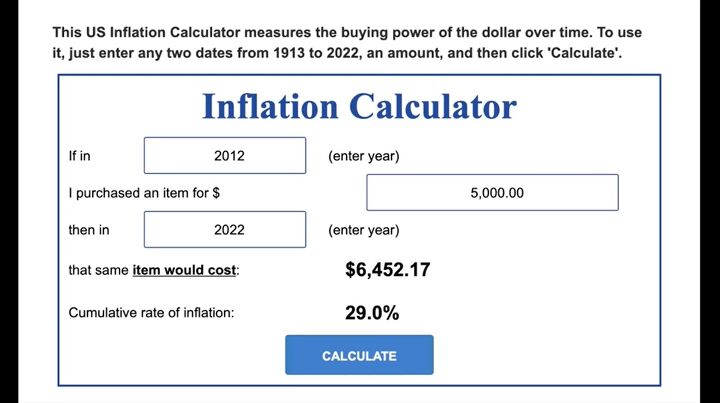

The rule of 300 does have shortfalls. One, it doesn’t indicate how your money should be invested. Two, it doesn’t factor in inflation. Let’s say you retired 10 years ago in 2012 and, at the time, were spending $5,000 a month.

Well, today, in 2022, you need roughly $6,500 to live at the same standards. That’s a pretty big variable.

2. The rule of 4%

The rule of 4% states that you need a nest egg large enough to live comfortably on 4% of its total value.

For example, if you want to live on $60,000 per year, you need investments of $1.5 million dollars. It’s similar to the rule of 300, but addresses annual, rather than monthly, income.

The rule of 4% addresses inflation. It says that in the first year, you withdraw 4% of your total investable assets. In each subsequent year, adjust the amount you withdraw by the rate of inflation.

So, if in your first year, you withdrew $60,000, and inflation sits at 8%, you would withdraw $64,000 the next year so that your purchasing power stays constant.

The rule of 4% also addresses investments, explaining that at least 50% of your portfolio should be in stocks. It banks on your investment slowly growing over time.

The rule of 4% also has its share of downsides and critics. For some retirees, investing 50% of their portfolio in stocks is too aggressive. Others think a 4% withdrawal rate is too aggressive or too conservative for their liking.

One of the founders of the 4% rule is actually now a proponent for adjusting the withdrawal rate to 5%. The rule of 4% only considers a 30-year horizon and doesn’t factor in taxes or fees.

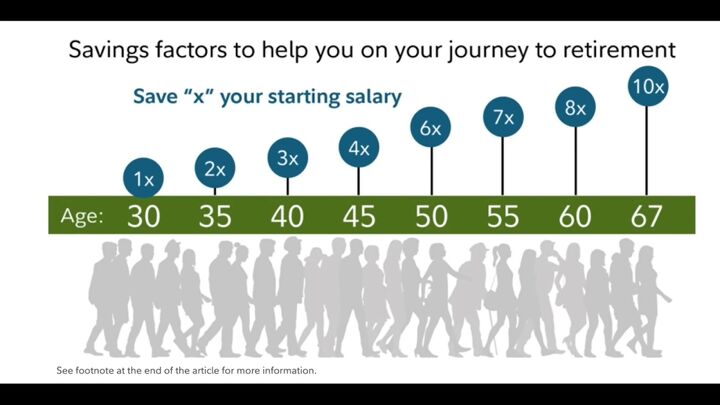

3. Savings by age

Another approach advocates hitting certain saving milestones by certain ages.

For this video, we will use fidelity metrics: you want to have 1x your annual income saved up by the age of 30, 3x your annual income saved up by the age of 40, and work up to 10x your annual income saved at 67.

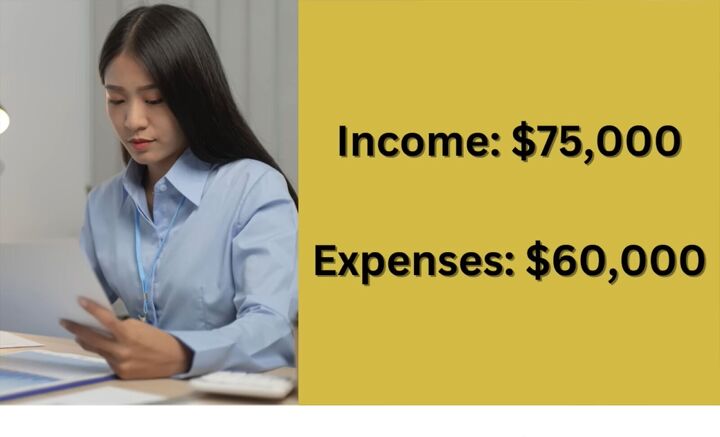

Keep in mind, this approach looks at income, not expenses. If we stick with some of the numbers we used previously, our fictional household spends $60,000 annually, with an annual income of $75,000, meaning they can save 20% annually. This household should have $750,000 invested by retirement age.

That’s literally half of what was guesstimated by the other rules. It’s worth noting that the ultimate amount will be based on your final income, which may be different at 67 than at 30.

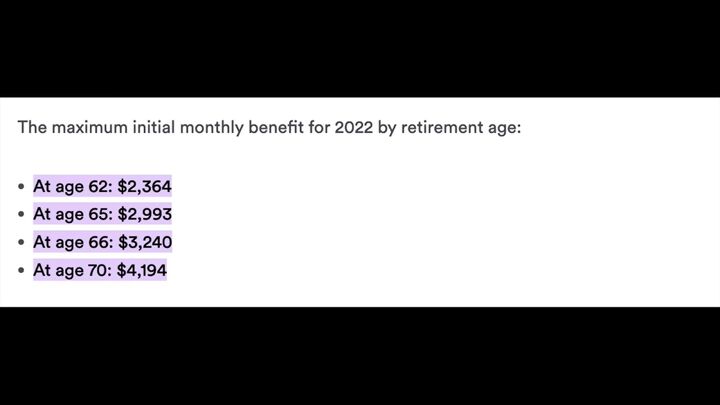

This number may be lower than other rules’ conclusions, because it looks at other income sources, like social security or pensions.

For most Americans, social security is a huge part of retirement income as you can see from this graphic showing the maximum social security monthly benefits at various ages. Failing to factor this in could mean you are saving way more than is necessary.

A big benefit to this rule is that it gives your little milestones leading up to an ultimate retirement goal. This keeps you on track.

4. Percent of income rule

The next rule states that you should have enough invested to replace a certain percentage of your income.

The percentage varies; some say you need 80% of your pre-retirement income, subtracting out the 20% you‘d set aside for retirement savings. Others argue that it can be even less because you are typically not required to pay Medicare or FICA tax on most of your retirement income.

Fidelity found that the typical retiree spends about 66% of their pre-retirement income. So, a household making $75,000 a year, would need about $49,500 a year for retirement. Of course, you will need to use other methods to figure out how much of a nest egg you would need to reach that kind of income.

5. The millionaire approach

The last approach is simple — have a million dollars.

It’s been a popularly cited number for decades. But, it’s the least thought-out approach. Just because people say you need a million dollars, doesn’t make it so. Whether or not you need a million dollars to retire, depends on so many factors.

How much do I need to retire?

All of these approaches are only general guidelines. Everyone’s retirement looks different, and it’s hard to know if your expenses will increase or decrease with time.

There are so many factors that make retirement planning complex, and kind of fun, for me. When it comes to saving for retirement, I follow the general guideline, when in doubt, save more, because I don’t want to run out of money.

What metric do you use? Let me know in the comments down below.

![101 Items to Get Rid of With No Regret [Free Declutter List]](https://cdn-fastly.thesimplifydaily.com/media/2022/08/30/8349390/101-items-to-get-rid-of-with-no-regret-free-declutter-list.jpg?size=350x220)

Comments

Join the conversation