How Can You Save on Vehicle Prices & What Car Can You Actually Afford?

Is your vehicle’s price too high? How much should you pay for your car? And, do you really need as many cars as you have?

The reason why you won't retire. It's your car.

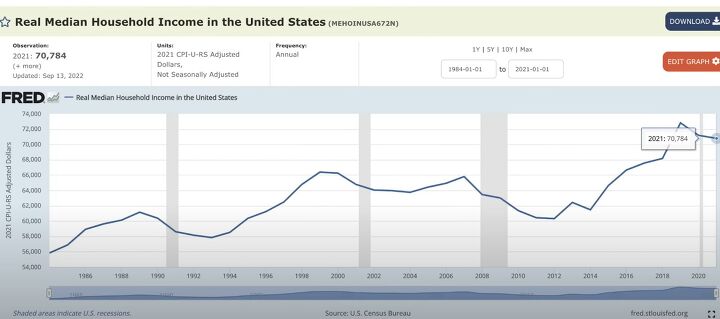

Average vehicle price

As of December 2022, the average vehicle price was $49,507. If we remove luxury vehicles, the average price was still $45,578. It doesn’t seem like there’s a heck of a lot of difference between luxury and non-luxury. The median salary for a worker in the US is $54,000. For many, a new vehicle costs close to what they earn yearly.

Looking at the household rather than individual income, the median is about $70,000. A new car is still a huge chunk for households with multiple income streams.

The 20/4/10 rule

We have some guideposts to answer “What type of car can I afford?” They aren’t perfect, but give you a good starting point.

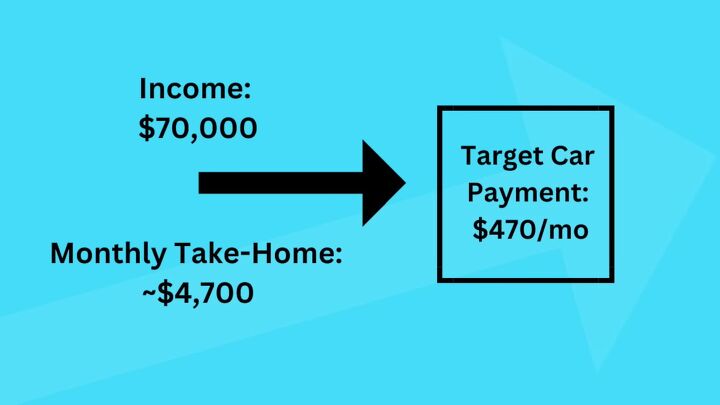

A vehicle payment shouldn’t be more than 10-15% of your monthly pay. This falls in line with the traditional car-buying rule of 20/4/10, where you put 20% down, and take a loan payment for no more than four years, which is no more than 10% of your home pay.

For a $70,000 income, your take-home is about $4,700.

Following this rule, you could afford a vehicle payment of about $470.

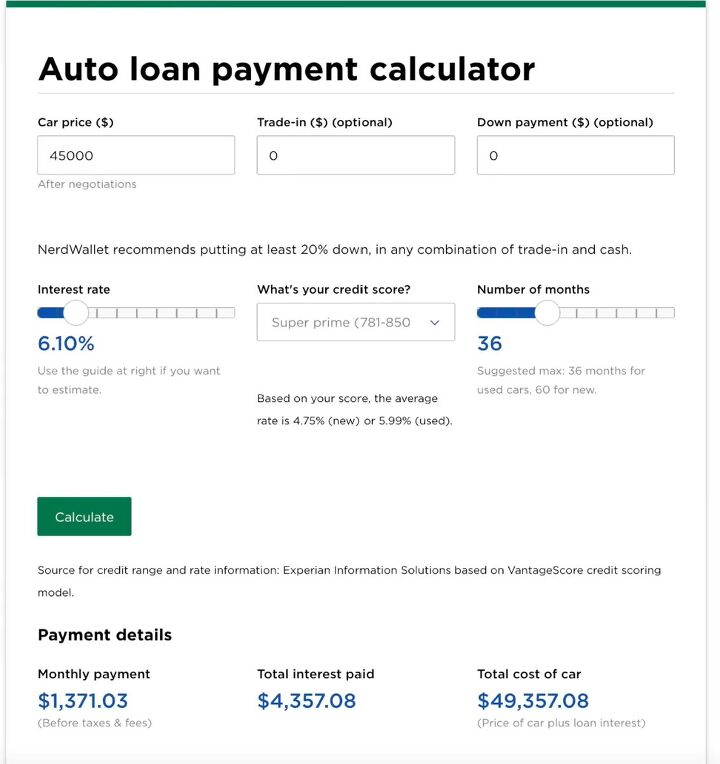

If you bought a new car for the average, non-luxury vehicle price of $45,000, assuming a great credit score and no down payment or trade-in, your three-year loan payment would be about $1,300 monthly.

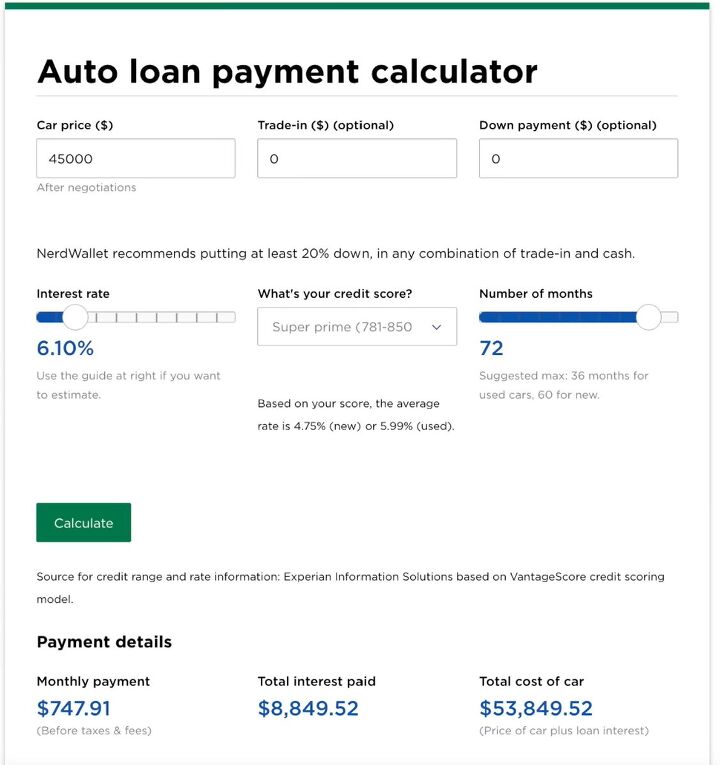

The most popular auto loan duration is six years. Even with a six-year loan, your car payment would be $750 a month — one and a half times what the car buying rule suggests, and it’s a lengthy commitment.

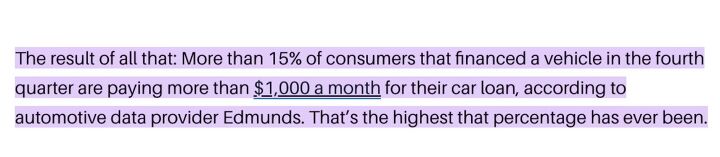

These numbers aren’t a stretch. 15% of new car payments exceed $1,000.

Buying a car outright

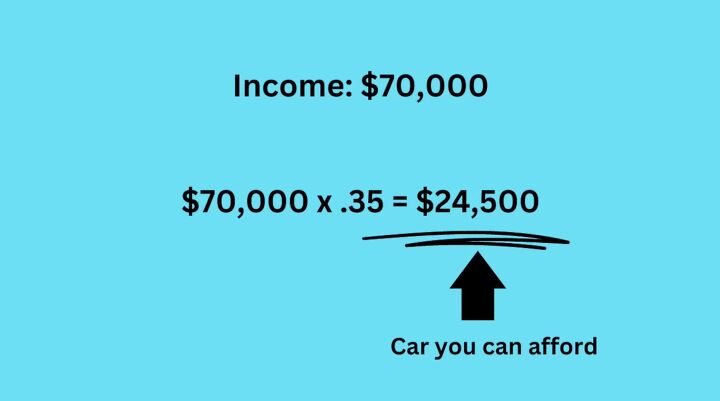

What if, instead of committing to a monthly payment, you buy a car outright? There’s a general guideline for that as well. Your vehicle price should not exceed 35% of your gross annual income.

For this rule of thumb, making $70,000, you could afford a vehicle price of $24,500 — a far cry from the prices we see on the market.

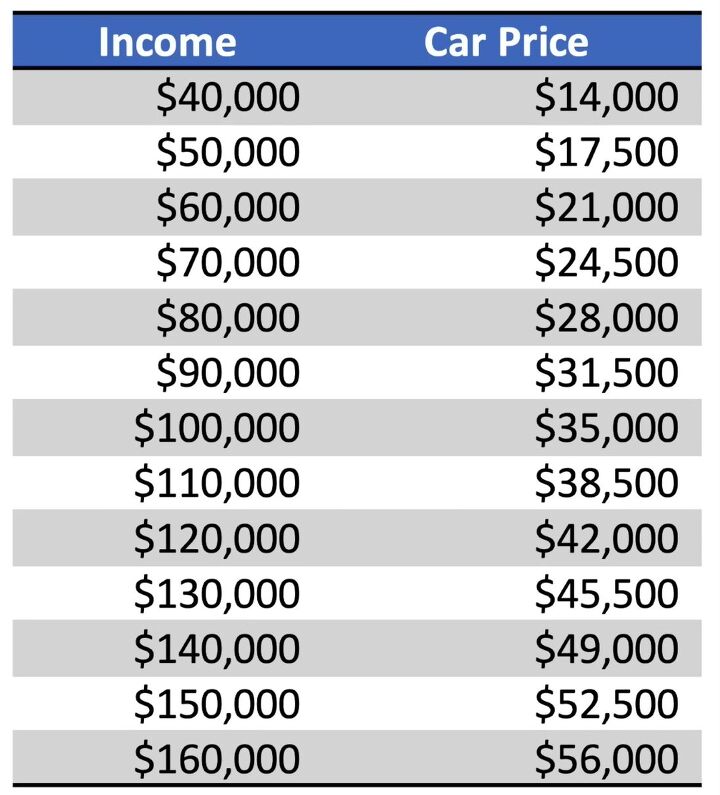

Using this 35% guideline, you’d need a household income of $130,000 to afford the average, new, non-luxury vehicle, or $140,000 to hit that $50,000 vehicle price benchmark, a salary that puts you in the top 75% of all households.

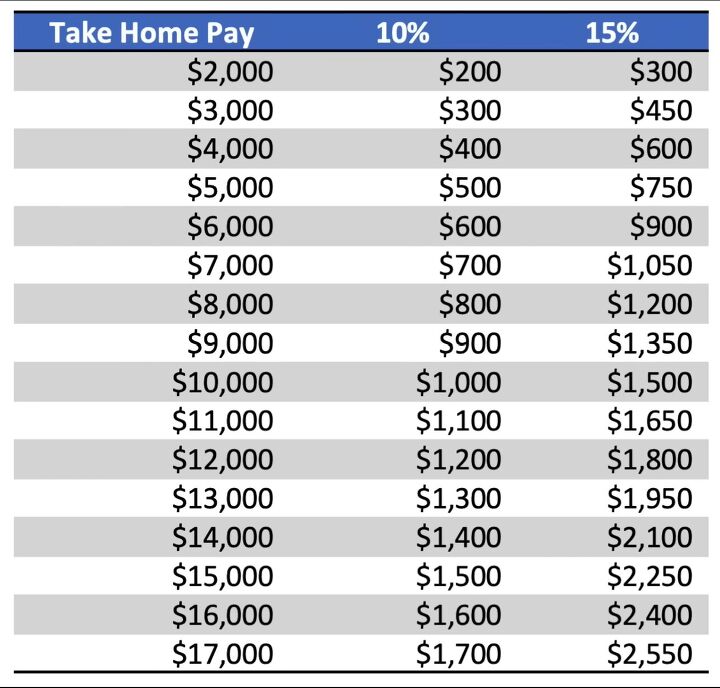

From the perspective of monthly payments, here’s what the rule of thumb gives as an acceptable vehicle payment.

The true cost of car ownership

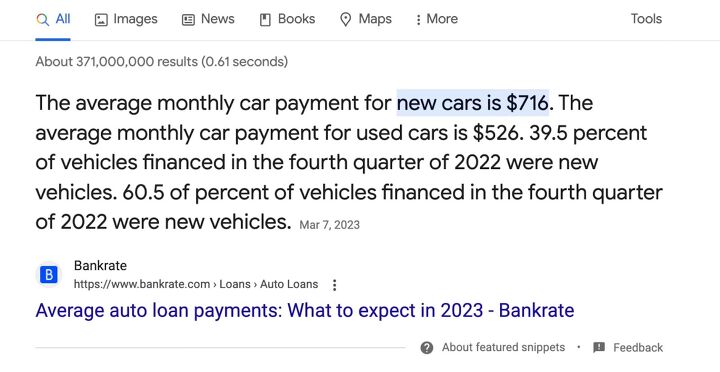

The average monthly vehicle payment on new vehicles is over $700 and over $500 on used cars. Many people extend their loan length to vehicles and simply ask themselves if the payment fits into their budget. You should look at the total cost, knowing the dealership can do funny math games to extend your payment to make practically any car fit with any budget.

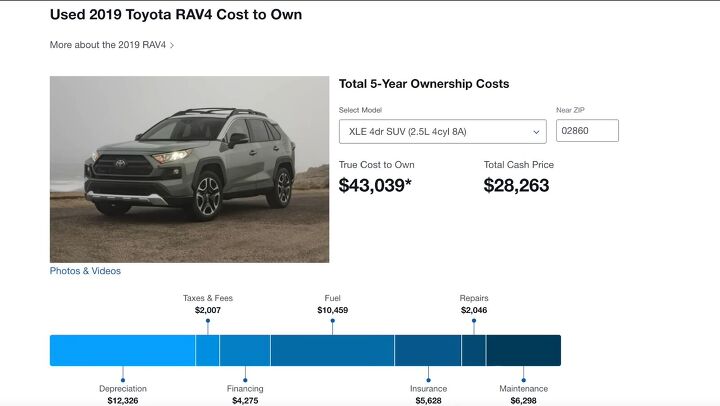

Also, consider the cost of car ownership. Cars come with expenses like insurance, licensing and registration, gas (or electricity), oil, routine maintenance, and parking fees. These costs add $500 a month to car ownership.

Edmunds has this calculator where you put in the car type to see the true cost of ownership. It’s incredibly valuable to see.

Spending your values

Every time we make a purchase or commit to a series of payments, we’re making a choice with our dollars. There’s nothing inherently wrong with how you want to spend your money, just know that you have a finite number of dollars, so choosing to do one thing is choosing not to do something else.

There’s no good, no bad, no right, and no wrong. You just want to allocate your money in a way that’s consistent with your values and meaningful for you.

Many of us can’t fathom life without a car. In many situations it’s essential. There are other situations where a car is a luxury. In a rural setting, a car is essential. If you live in a city with a well-established transit system, it’s a different world.

Maybe you need a car, but do you need multiple vehicles? Some families have three cars and only two drivers. Ask, “Could we get by with just one car?” Maybe yes, maybe no. Only you know your situation.

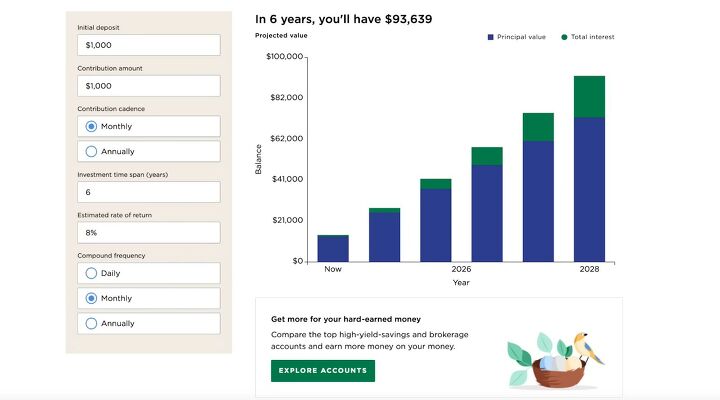

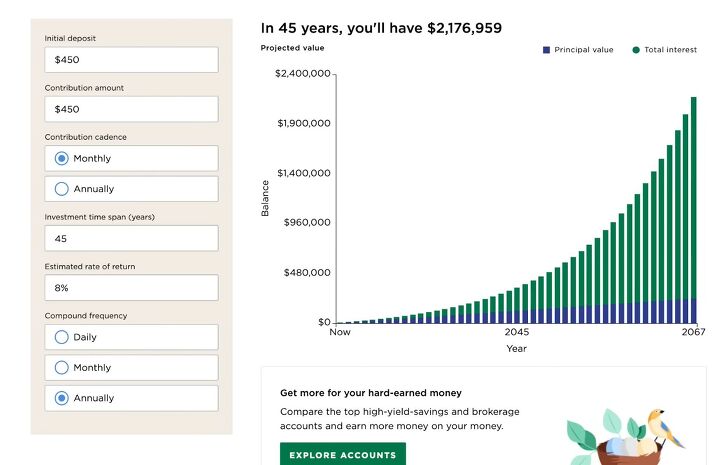

What if the extra car had a $500 monthly payment and $500 in monthly expenses? If, instead, you took that $1,000 dollars a month and invested it for six years (the length of a typical car loan), it would grow to almost $100,000. Would you prefer a depreciated asset or a start to a nest egg?

If you left the money alone for 30 years, it could turn into seven figures! Is your vehicle the reason you’re living paycheck to paycheck or delaying retirement?

Saving on your car

You can certainly argue you need a vehicle to get places, but, do you need to do these things in a Mercedes? Probably not.

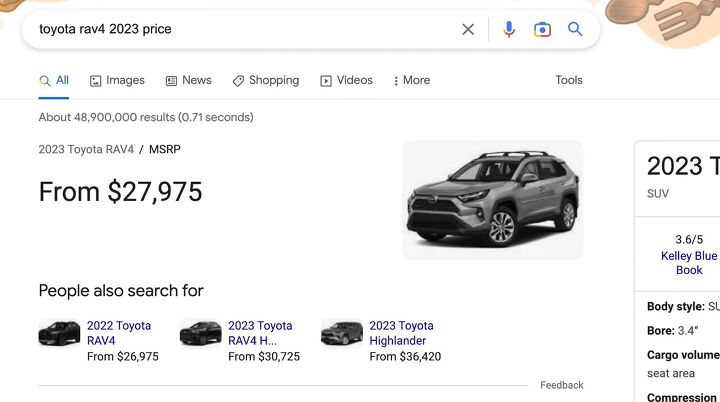

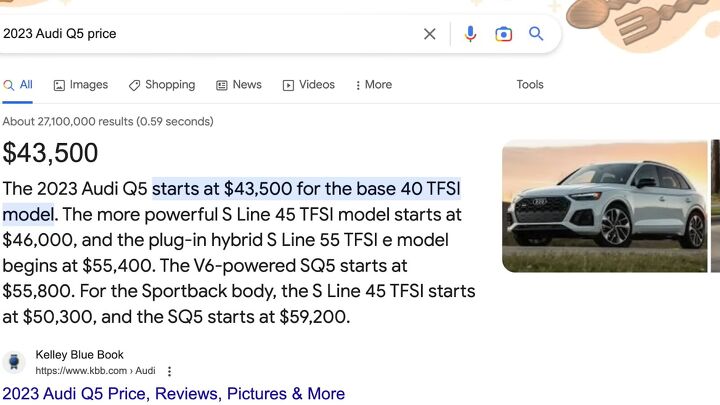

Say you’re debating a new car. You’re looking at the Toyota RAV4 ($30,000) and the Audi Q5 ($45,000). All other factors being identical, the difference in monthly payments is about $450.

$450 invested every month makes a pretty darn nice retirement nest egg.

How can you save on vehicle prices?

Buy used cars. New cars lose 20% of their value in the first year and 15% each following year. A car in the 3-5-year-old range gives you big savings and a nice car with lots of life left.

Even if you’re happy with your insurance, put some feelers out. Here’s why. If you’re not shopping around, the auto insurance companies share that with each other. They know you’re not looking and will start to incrementally raise your rates faster.

If your credit score is subpar, hold off on buying a vehicle. Auto loan interest rates vary based on your credit score.

Keep your car for a long time. Ideally, you want the life of your auto loan payment to be short and the life of your vehicle to be long, so you can enjoy time without a car payment.

What do you think about the average vehicle prices? How much did you spend on your car? Let me know in the comments.

Comments

Join the conversation