What is the Best Age to Take Social Security?

Social Security is a huge factor when it comes to retirement for many Americans. This means that many people wonder about the best age to take social security. How do you know what's the best age to take Social Security?

Ages for Social Security

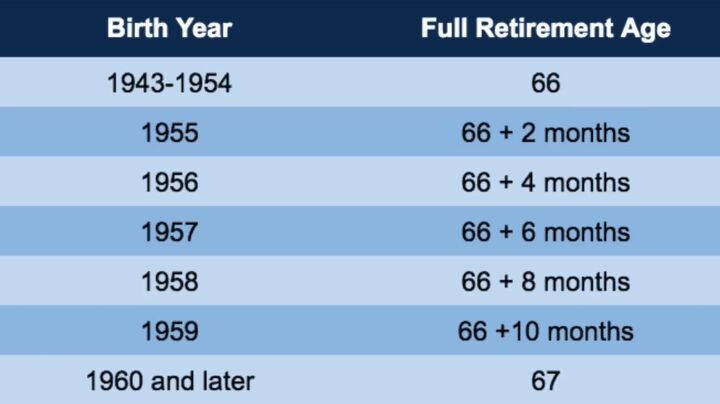

There are two primary ages when people are most likely to take it. One is early at the age of 62, and the other is full retirement age, which is either 66 or 67, depending on when you are born.

You can delay taking until 70, thereby further increasing your benefits but only a small percentage of people do this.

Claiming before the full retirement age reduces your benefit, and claiming after the full retirement age increases your benefit.

Reduced benefits by age

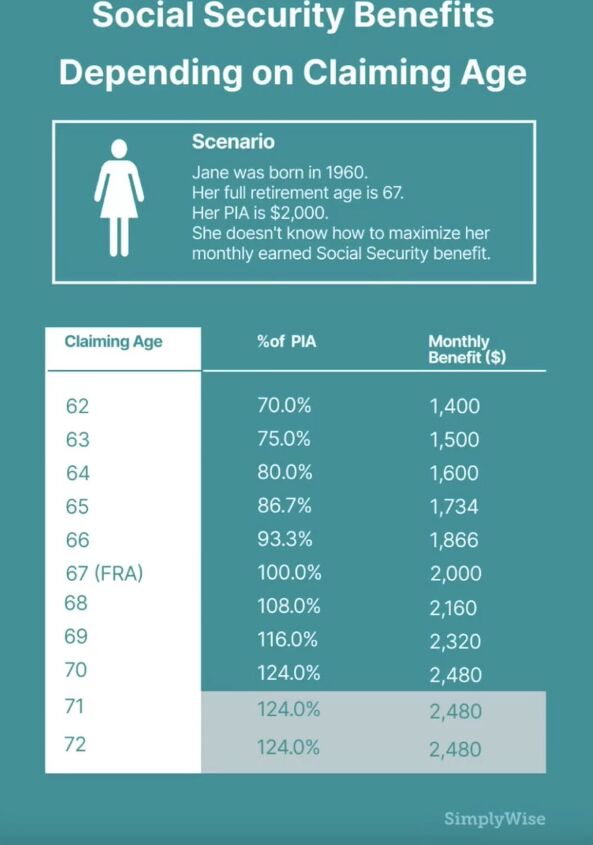

Claiming early at 62 will reduce your benefit by 30% of your full retirement age.

Delaying claiming until 70 will increase your benefit by 24% of your full retirement age amount. Now, at first glance, it may seem like a simple question - like what's the best age to retire?

As with most financial questions, it's far more complex than simple surface level. It involves a lot of deliberate thought calculations, the best guesstimate on your life expectancy, and analysis of opportunity costs.

Ultimately, it's a personal decision about what's best for you and your life circumstances.

What if we were to look at it strictly from a mathematical perspective and ask the question, what's the best age to claim Social Security? For this example, we are going to use 67 as the full retirement age.

The break-even point

The earlier you collect, the lower the benefit you lock in, but over a longer time horizon.

There comes a break-even point, a point where the total lifetime amount you receive from Social Security is greater if you delay collecting your benefits to full retirement age or even delayed retirement age.

That break-even point hits at age 79 if you compare collecting at 62 versus 67, and the break-even point hits at age 80 if you compare collecting at 62 versus 70. The break-even point hits 81 if you compare collecting at 67 versus 70.

You can make statements like if you were to pass away any time before the age of 78 or 79, you would be better off collecting Social Security early at the age of 62.

But if you live to the age of 82 or beyond, you're better off delaying collecting your benefits until the age of 70 in terms of net benefit received.

Opportunity costs

If you retire at 62, odds are you're going to need an income source of some form, whether that's coming from Social Security or your investments.

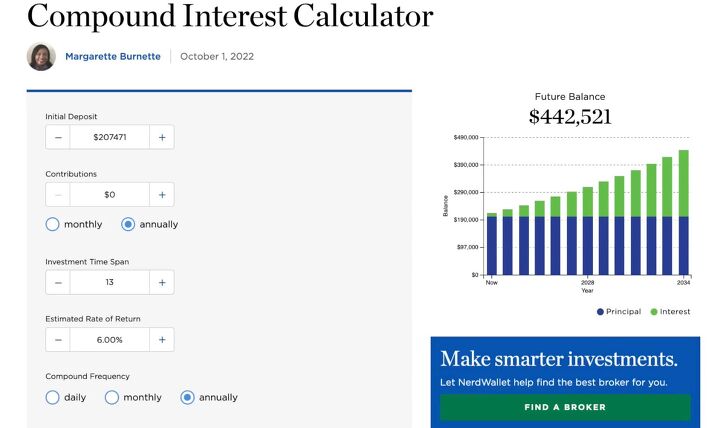

So let's look at opportunity costs. Let's say we have a retiree who retires at 62 but doesn't draw Social Security. They're allowing their benefits to increase. Instead, they withdraw from their investments the same amount that they otherwise would have received from Social Security.

In this case, delaying taking your Social Security and drawing on your investments has a pretty big opportunity cost. In terms of what you were able to draw out and what that money would have otherwise grown to, that's a difference of $37-51,000, depending on your rate of return.

From a numbers perspective, drawing Social Security early and leaving your money invested seems to allow you to come out ahead financially.

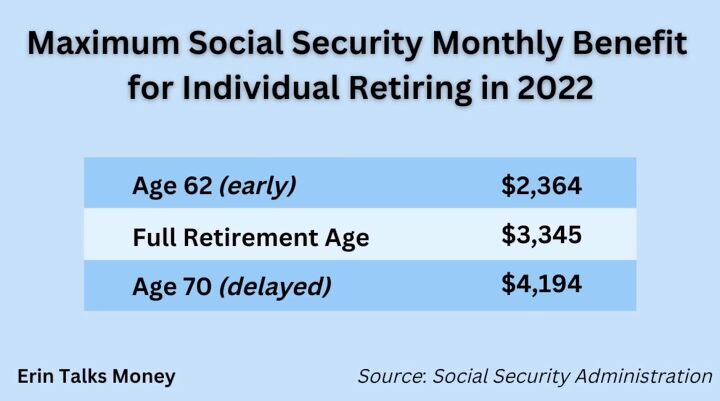

Claiming Social Security at the age of 62 is the most common age, simply because that's the earliest age at which people can claim.

Cost of earning additional income

Now, there are other implications to consider. If you draw Social Security at 62, if your full retirement age is 67 and you decide to draw at 62, the benefit amount that you receive will be reduced by 30%.

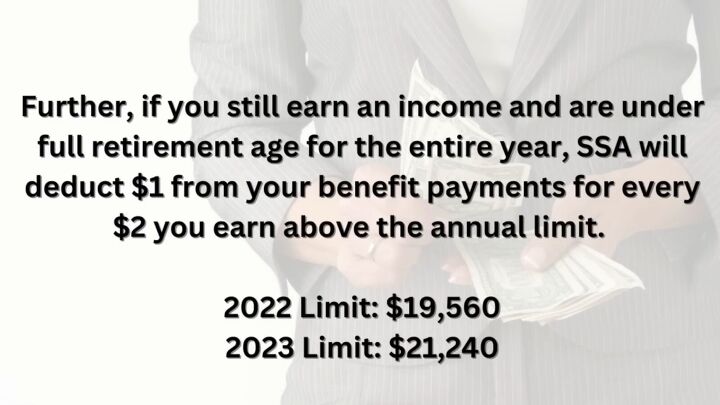

If you still earn an income and you're under full retirement age for the entire year, the Social Security Administration will deduct a dollar from your benefit payments for every $2 you earn above the annual limit.

So that means you can earn up to that amount without your Social Security benefits being affected. However, if you earn over that amount, your benefits will be reduced accordingly.

Keep in mind that any money deducted from your benefit is not permanently lost. After you reach full retirement age, Social Security will recalculate your benefits and increase them to account for the benefits that it withheld earlier.

Once you reach full retirement age, there's no income restriction.

Let's say you want to work past the age of 62. You get fulfillment from your job and the engagement it brings. Let's say that your income will be significantly higher than those threshold amounts. Well, in that case, drawing Social Security early wouldn't be a wise choice.

Ultimately, when you should draw Social Security heavily depends on your situation. No blanket statement can be made saying it's best to draw early or it's best to delay filing. There are so many

factors to consider.

If you decide to work until full retirement age and delay collecting Social Security until that time, you're entitled to 100% of your full retirement benefit. You lock in a higher monthly benefit.

Retirement goals

The net benefit received isn't the only factor to consider. Locking in a higher benefit, which could be as much as $1,000 per month higher by claiming at full retirement age could be a big deal.

At the very least, it's going to be several hundred dollars. You have to ask yourself, would this extra monthly money allow you to do things that you want to do in retirement? If the answer is yes, then maybe waiting till full retirement age is the better age to start drawing.

You have to ask yourself those similar questions if you're considering delaying till 70. Deciding when to take Social Security is based on so many different questions, many of which are impossible to know the answer to.

How long will you live

Most glaringly obvious is when will you pass away? As morbid as the question may be, it's one of the most important factors to consider. Because if you pass away before the age of 78, 79, or 80, depending on what your monthly benefit is, you're almost always better off having drawn early.

In terms of net benefit received, I say almost always because there are situations in which people prefer to continue working and delay collecting so they can lock in a higher benefit.

When you're looking at a ten or a 20-year time horizon, inevitably there's going to be some gray area there. Numbers are black and white, purely analytical, but the people who interpret them aren't. So this will influence your decision on the best age to take social security, specifically for you.

The best age to take Social Security

What do you think is the best age to start drawing Social Security? Let us know your thoughts in a comment down below.

Comments

Join the conversation