How to Work Out the Best Family Budget Method For You

Our family is done fighting over money. Staying on a budget has saved me money, sanity, and my marriage. I’m going to go through a few family budgeting examples.

Budget line items that cost more

Here’s what a typical week looks like for me–visits to Home Depot, Walmart, Costco, and Target. Like take Home Depot–I will go in there with a specific project in mind that should cost $20 to fix.

But by the second or third trip to Home Depot–after buying another couple of $5 parts–sometimes the cost gets out of hand. I’ll justify it by thinking it’s a one-time thing, but those one-time projects turn into frequent every-other-month projects.

Spending habits

Maybe Home Depot is my budget item line weakness. For my wife, maybe it’s Costco or Target.

Maybe you go in there for a $35 trip to buy one bag of dog food but $350 later, there are new Halloween costumes, new clothing, new supplements we need to try, or new groceries–all in the basket with the dog food.

There’s a difference there between our spending habits. Getting on the same page about spending projects is the first priority and most helpful thing for your family as it is for mine.

Finding that 1 percent inefficiency in our budget

Only 32 percent of U.S. households prepare a monthly budget. If the average family was 1 percent more efficient in their budget, they’d retire with $100,000 more money.

So, here’s how to get to that number.

Let’s work with one percent of efficiency on a $50,000 income–which is low–the average is about $62,000–but if we’re just looking for simple math, we’ll use a $50,000 income. So for a $50,000 income, we will have $500 that’s an inefficiency.

So, maybe at the end of the year, you find yourself with $500 extra dollars because you fixed that inefficient part of the budget. You will put that money away once a year–just once a year. By doing that, over the course of 30 years, you would end up with around $100,000 more in your pocket just by investing it.

Little bits of money over a long period of time can compound and grow and that’s why you want to look at your budget. Now, let’s look at some budgeting examples.

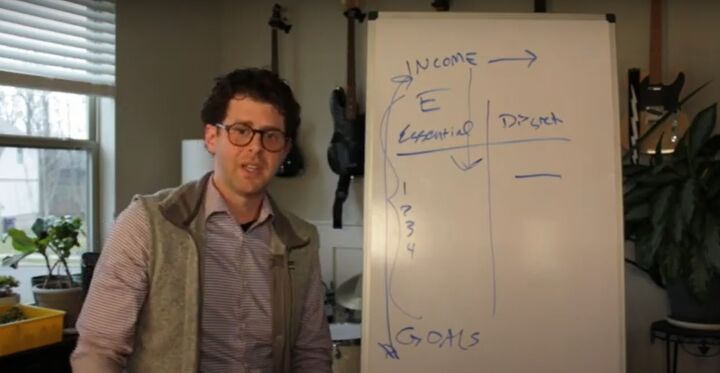

Budget option 1: Bare-bones 2-column budget

Use two columns for this budget. One column is “Essential” and the other is “Discretionary.” Essential is housing, transportation, clothing, and food. Discretionary is everything else and this is where you get into a gray area of what’s discretionary food, for example, and what is essential food.

There are basic rice and beans to more discretionary Doordash orders and fees. In my opinion, Doordash is completely discretionary.

Your income–which is your paycheck plus every penny you pick up along the way–is listed on top so you can see it clearly. At the bottom of the page, you list your long-term goals–but start small and build them up every month.

This is how wealthy people become wealthier–by making their income serve the purpose of their goals, which are buying and investing in assets.

Budget option 2: More detailed 2-column budget

Here you are detailing your two columns, breaking them out into specifics plus goals for each. I suggest picking six to 10 categories to break out and monitor more to see where your money goes.

For example, take utilities. Your utility costs go up and down depending on usage. It may sound obvious but this is one category where people are always surprised by how much more they’re spending. The second surprise category is usually groceries.

The envelope system

A budget is a permission to spend, but it’s also a tool to help you see where you can cut back week to week or month to month.

If you find yourself stressed out in line at the grocery store over whether you can afford a giant package of toilet paper, think about if you really need it or not. But if you know you have money set aside for that, then it can be liberating, not stressful, to buy it.

A great way to start a family budget, in the beginning, is to use the envelope system. You literally go to the grocery store with an envelope.

Yes, this is an old-fashioned way of budgeting, but it works. You just won’t spend more than what’s in that envelope. Your categories will be specific to you in addition to food.

Budget option 3: Zero-sum budget

This option shows you how to max out putting every dollar to work when money comes in. The categories go beyond essential or 10 categories but we have a zero-sum budget where every bit of income has a specific role.

This is a budget for the long-term mindset. It’s not month-to-month thinking anymore, but it’s more six to 12 and 18 months of planning.

Sinking funds

What is a sinking fund? This is when you are taking money, setting it aside, and letting it build up in a fund for auto maintenance, for example. But I have peace of mind because I know that I have money going monthly to a sinking fund to take care of new tires or brakes.

The fund is built up and depleted when needed, but you rebuild. Other sinking funds are big bills like insurance, or down payments for large items, such as a house.

Ways to budget for a family

What you really want to do is examine your transactions over a one to five-year cycle. If you’re getting into the habit of budgeting on a monthly basis, you’ll really get a good sense of what to do for long-term goals.

Just keep a routine going–review your budget with your spouse, put every dollar to work (even $20!), and avoid debt by just spending the money you have, not spending what you think you may be getting next month.

Let me know in the comments if this makes sense to you as a way to start a family budget and stop fighting with your spouse about money.

Comments

Join the conversation

Very practical advice. 👌