How I Set Up Sinking Funds to Save the Most Money

Hey everyone! I’m going to talk to you about how I put together my family’s sinking funds. I get so excited talking about sinking funds because they have completely changed our finances. If you are unfamiliar with sinking funds they are basically just planned savings.

I’m going to show you some of our sinking funds and explain to you how I came up with the numbers for our goals. There are two types of sinking funds. There are date certain sinking funds that need to get paid on a specific date. Then there are perpetual sinking funds.

Perpetual sinking funds are sinking funds you save for all year long no matter when the expense arises. Christmas is complicated for us because even though it has a date we treat it like a perpetual sinking fund and try to save for it all year round. Here are some of our yearly categories along with explanations of how I got my numbers and how I plan my savings.

Table of contents

1. Examples of sinking funds details for Christmas

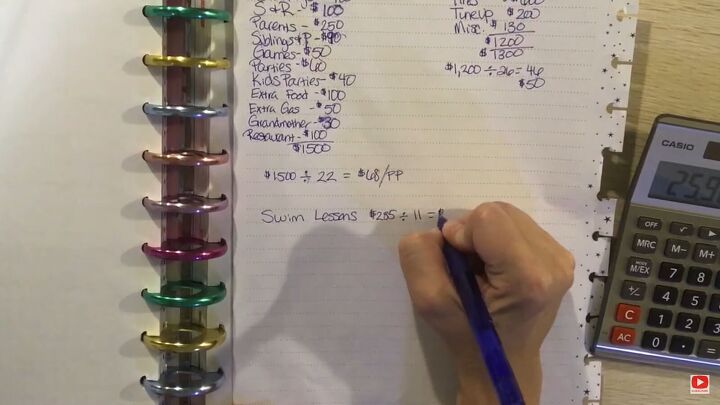

One of the most important steps in figuring out your sinking funds is assessing the number of pay periods for a certain fund. Using Christmas as an example, there are 22 pay periods from January to October. If we have a $1500 budget for Christmas we will have to save around $68 dollars for Christmas at each pay period.

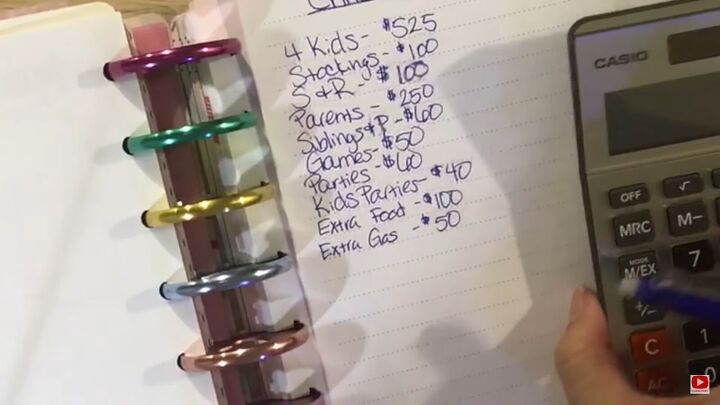

I used to budget $100 for each of our 4 kids but that has become too small a budget as our kids grow older. We give them each 3 gifts from Santa and 3 or 4 gifts from us. Our older girls are starting to want more expensive things. We decided to raise the budget for the two older kids to $150 each and $100 and $125 for the little kids.

Now I know I need $525 just for their gifts. I’m putting aside a separate $100 for stocking fillers. Then we also budget $50-$100 for gifts for me and my husband.

When it comes to people outside of the immediate family, I think it’s a good idea to list out each person you’re going to buy for and have a budget set for each of them. We also budget for parties for the kids and for the adults. Then we always budget $50 for extra food and $100 for extra gas at that time of year. I also add $50 for restaurants.

When I total up all my expenses I see that I will need to budget $1500 for Christmas this year. That would be an additional $300 on top of our usual budget, which is a bit steep so I think we’re going to have to do some things to bring that number down. Maybe we’ll focus on making some handmade gifts.

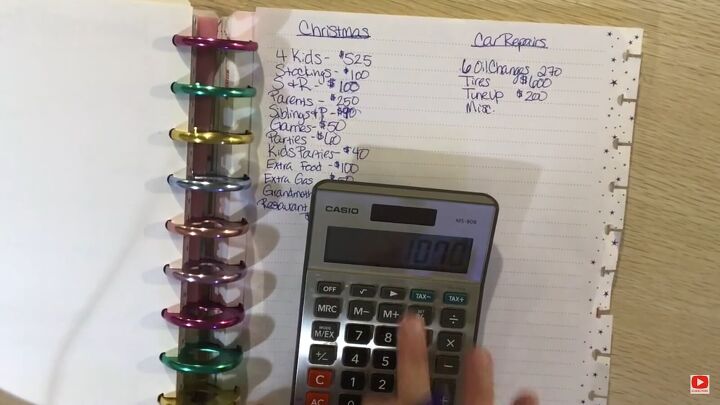

2. Planning for car repair savings

We have two older vehicles so we’re probably looking at a total of 6 oil changes a year. That runs us about $40 each. I also know I will need new tires which will be around $600. We’ll also need to budget for a tune-up and miscellaneous because you just never know with cars. All in all, I came up with a $1200 budget for cars.

Car repairs are another one of those perpetual savings envelopes. I divide the $1200 by 26 for the 26 pay periods and now I know I have to save about $46 for car repairs during each pay period. I decided to round that up to $50 a pay period giving us a bigger budget for miscellaneous.

3. Date certain sinking funds

I know I need to have all of the money for the girl’s swim lessons saved up by June so this is a date certain sinking fund. This means I need $285 from the 11 pay periods I have until the end of May. I now know I have to save $26 per pay period for swimming lessons.

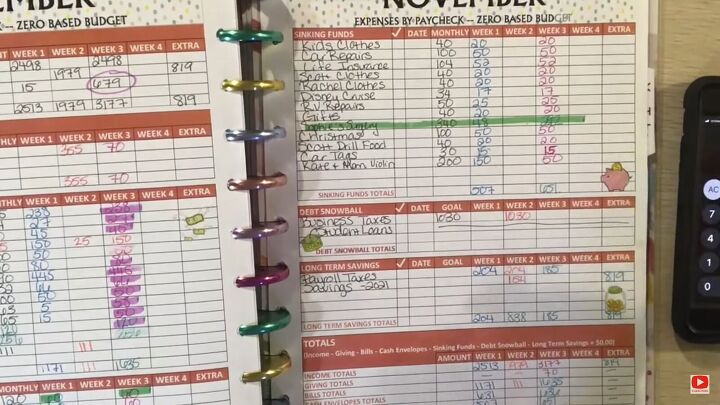

I would recommend you have a subscription sinking fund. We also have sinking funds for home repairs, vet bills, kids' clothes, and school fees and supplies, just to name a few. The more detailed you can get when planning your sinking funds the easier it will be to maintain and manage your budget, so get specific.

4. The general idea

These are the general principles you need to apply when figuring out your sinking funds. Figure out your categories, how much you will need for each category, and when you will need it. Then figure out how many pay periods you have till you need to reach your goal and determine how much you need to set aside from each pay period.

Going over my sinking funds I am realizing that we are not bringing in enough money for all of our expenses so I’m going to frontload or put more money in the sinking funds that are due the first half of the year. We have a lot of expenses that we’re going to plan for so I probably won’t start working on Christmas until July this year.

Instead of putting in the same amount every single pay period in each fund like I did last year, I’m going to be putting larger chunks into different sinking funds each pay period. Your sinking funds will need to be adjusted and rearranged according to the numbers and information you gather around each category. It is something you need to check in on and manage according to your changing needs.

Sinking funds

I love sinking funds because we manage our money so much more efficiently when we have a plan. It requires a little more effort up front but it saves us so much money and relieves a great deal of stress. Let me know in the comments what you save for in your sinking funds. I am always so interested in how other people do their budgeting.

Comments

Join the conversation