How to Create a 2023 Budget & Reach Your Financial Goals

I'm a strategic money coach and I am going to help you create a 2023 budget. When we’re more intentional with our money we can do more of what we want. It doesn’t matter what your income is. You can create a budget that helps you strategically decide how you want to spend your money before you get it.

Today is a great day to start better managing your money. What you did with your money in the past does not dictate your future habits. All you need is a calendar overview and a few sheets of paper.

We are going to be budgeting monthly. A monthly overview will help you see how much money you're going to be receiving and how much you’re going to be spending on bills, expenses, savings, and anything that you spend money on. We are creating a zero-based budget, which means every dollar has a purpose.

There's no such thing as extra money. If you are anticipating receiving money, it should be managed and given a purpose. Money flows where there is a purpose. If you don't give the dollars a purpose, you will spend them recklessly.

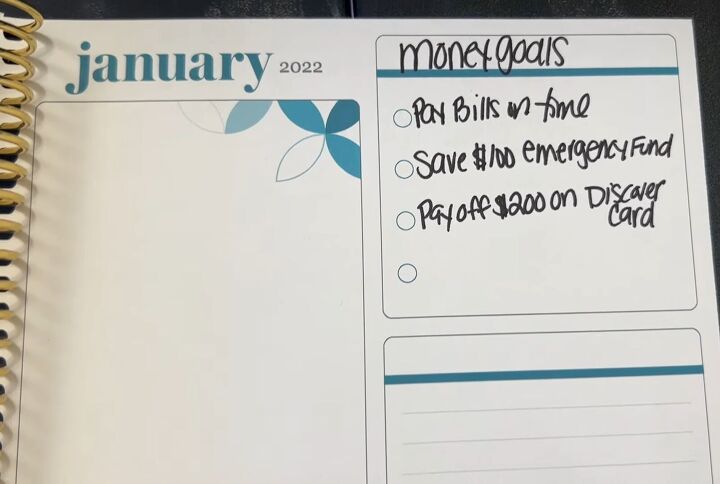

1. Write down your goals

For our mock budget, the goals are to pay bills on time, save $100 in our emergency fund, and pay off $200 on our credit card. Writing down your goals creates a focal point. For every dollar you spend, ask yourself if it’s getting you closer or further away from your goal.

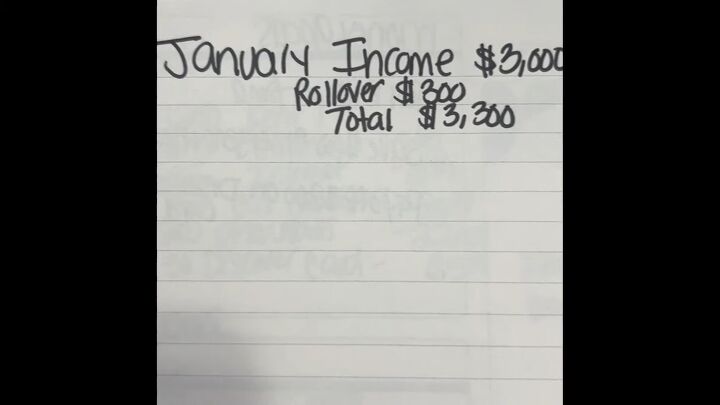

2. Figure out your income

At the top of your page, just underneath your goals, write your monthly income. If you have any money left over from the previous month, that is called rollover.

Write down that amount as well. You may have a rollover because you didn't use up all your expenses, or you have bills due the following month. If your income varies, budget on average, off your lowest average.

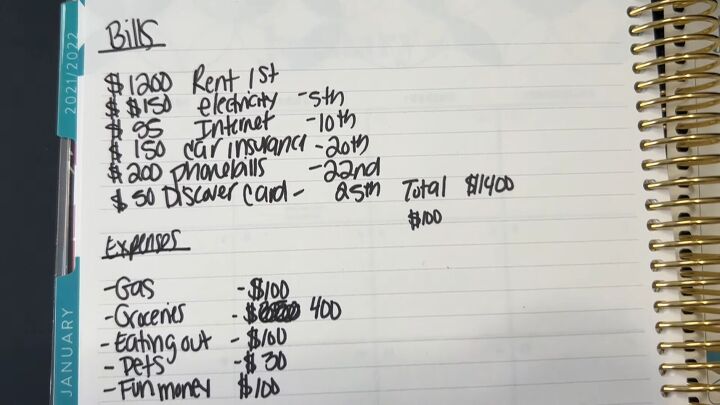

3. Know your numbers

Figure out how much money you need to pay your bills. Bills are anything with a recurring due date. Rent, car payments, your kids’ soccer, and anything else that has a due date is a bill. Write down the name of the bill, the amount, and the due date.

The due date is important because you're going to put everything in your calendar so you can clearly see which bills are due and when. If you don't know how much you pay in bills you can look at your bank account. If your bills fluctuate, take the average of the past three months. Budget based on your average and a little extra just in case it fluctuates.

After you’ve written down your bills, go through your expenses. Expenses are anything that you spend money on that doesn't have a due date. Things like gas, groceries, and date nights are all expenses.

Assign each category of expenses an amount that you want to spend. I call these baby budgets.

When you know exactly how much you have available to spend you find ways to stick to the budget. You shop sales, and deals, and use coupons to stay under budget. Don't let the prices at the store dictate what your grocery budget is.

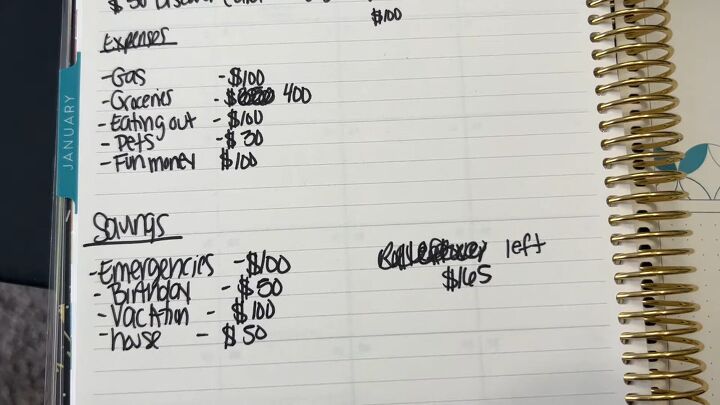

4. Savings funds

Everyone needs savings funds. You need savings for emergencies or unforeseen expenses. Maybe you want to create a savings fund for vacations or an event. Your savings need a purpose.

Take your income and subtract your expenses, your savings, and your bills, and see if the numbers add up. If your monthly income is $3,000 and your bills and expenses come to $3,200, that means you don't have enough money coming in to cover everything. Go back to your expenses because that’s where you have the most control.

If it's the opposite, and you're $200 under budget, you need to give that extra $200 a purpose. You can allocate it to savings. It could go into your cushion fund, so you have money to cover next month’s bill. It doesn’t matter how you spend it as long as you have a plan and an intention for it.

5. Planning paycheck to paycheck

Now that you have your monthly overview, break everything down from paycheck to paycheck. You need to know what you're doing with your money when it comes in.

You can decide to pay bills and rent with paycheck number one and add to your savings with paycheck number two. Each paycheck should have a focus. This way, when you sit down on payday, you know how to allocate your money.

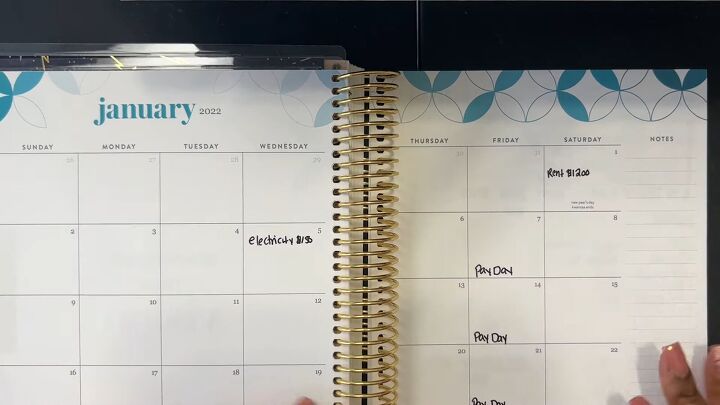

6. Put everything on the calendar

Write down your bills and income dates in your calendar. This serves as a visual reminder so that you can see what you need to pay and when. It will help ensure that your bills get paid on time, and it will prevent you from overspending.

7. Check in weekly

Check these numbers on a weekly basis. On your paper, write each expense, the date, what it was for, and the amount. It’s important to do it once a week, minimum. It will allow you to see if you’re sticking to your budget.

If you’re already halfway through your grocery budget and it's only the 10th of the month, that's an indicator that you’ve got to slow down. Figure out where you’re going to pull that money from. You may need to adjust other expense categories to make up for overspending.

8. Set a budget every month

Things are going to fluctuate every month. It's not something you can set and forget. Your budget is a living, breathing document that you need to tend to regularly.

How to create your 2023 budget

I hope this advice helps you set up your budget and better manage your money. Budgeting will enable you to add to savings accounts so you can do more of what you want in your life.

If you want more help with budgeting and intentionally managing your money, reach out to me in the comments.

Comments

Join the conversation

This still works today.