How Much Do I Need in a Rainy Day Fund? - Be Recession Ready

Many people wonder, "how much should I have in a rainy day fund?" I will go over that so you know what the average rainy day fund should consist of. A rainy day fund is an emergency fund, so you're prepared for unexpected expenses that can put you into a financial crisis if you aren't prepared.

There are five things to consider to figure out how much you need in your emergency fund.

1. Figure your living expenses

The first thing you need to do to determine how much of a rainy day fund you need is assess your living expenses. This is different from your monthly budget because your monthly budget includes all those extras you enjoy every month. These are your bare-bones expenses, not discretionary funds.

The emergency fund is your pared-down amount of what it would take to keep you alive and in heat, housing, and necessities.

As soon as you figure out how much it would take to cover all your living expenses, you know how much a month's worth of a rainy day fund would be. The general recommendation is to save three to six months' worth of living expenses, which you just figured out.

2. Decide if you need more than 3-6 months of expenses

The next step is to decide if you need more than three to six months worth of expenses because of what your life is like. Some of the reasons Vanguard gives to have more in your emergency savings are during a recession because unemployment rates can be higher if you're in a high-risk industry for layoff.

Also, consider having a larger rainy day fund if your income isn't steady or you are retired and living off investments. You might want to consider having more than just a three to six months emergency fund in your savings account in cash.

Bankrate added a few more ideas about when you might want to have more in your emergency savings. If you're self-employed, you might consider having more emergency savings. If you're self-employed, you need more because that income can be variable, and it depends on you and your health and your well-being for that to work to keep bringing money in for you.

I have a lot of food allergies, which can make eating more expensive. So we account for that when considering how much of a rainy day fund we need. You need to account for those essential medicines or supplements for your health.

3. Decide if you need less in your rainy day fund

Next up is to consider scenarios where you might want to have less in your emergency savings. Bankrate had a few ideas about when you might want to save less in your emergency savings.

Those would include if you don't have very many expenses. Maybe you have your house paid off or don't have a payment on your car, or you don't even have a car, so you don't have to worry about maintenance.

Maybe you've kept your expenses low, so you don't need as much emergency savings.

Maybe you don't have any dependents. Perhaps no one is relying on you. If you have children, you need to have enough in your rainy day fund to cover all their expenses.

Also, you may not want as much in your rainy day fund if you have credit card debt. If you're dealing with high-interest credit card debt, it may not be worth it to have all your money in your savings account where it's not doing you any good. Instead, it could save you tons of money in interest if you throw all your emergency savings towards your credit card payoff.

This goes along with how Dave Ramsey thinks. He says you should save just $1,000 for an emergency fund and start tackling your debt. This goes before building that three to six months' worth of emergency savings.

Maybe $1,000 isn't quite enough, but it's something. If you're focusing on paying off that debt, it might not be the wisest move to have a ton of emergency savings.

Also, You may not want as big of a rainy day fund if you're trying to focus on planning for retirement and saving for that. I don't know about every single retirement account, but most retirement accounts allow you to take out the principal in an emergency. I definitely wouldn't recommend it if you could avoid it.

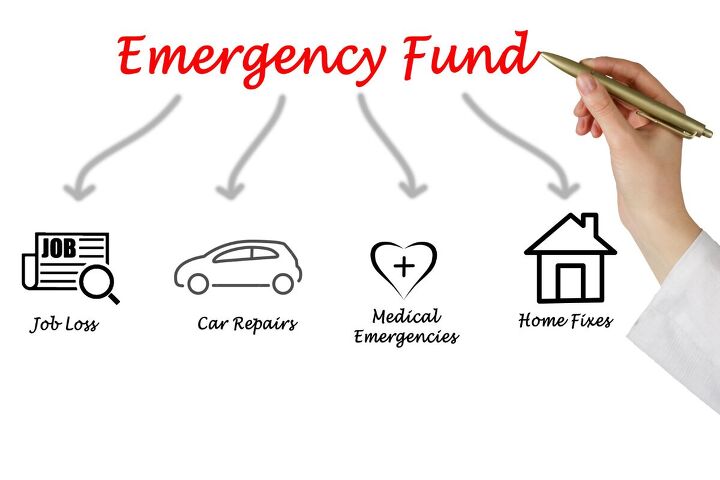

4. Define your emergencies

Next up, to figure out how much emergency funds you need, you need to consider what this money could be needed for.

What things qualify as an emergency for you, and what would that look like? Maybe an unexpected car repair that's $1,000. Or perhaps an unanticipated extra medical expense that could cost thousands of dollars.

Possibly your rainy day fund would be used for the loss of a job. You would use that rainy day fund money to live off of. You also may plan on your rainy day fund to transition from a job you don't like to a job you want.

5. Set realistic expectations

Lastly, remember when building your rainy day fund that something is better than nothing. Maybe all of this sounds so daunting. You start calculating your living expenses, thinking three months' savings sounds impossible. That sounds like so much money. I can't imagine saving

that much.

How much should I have in a rainy day fund?

Start small and do what you can now. Maybe it's not ideal. Life is never ideal and never perfect. Save money to put into the rainy day fund that you can now, and don't worry too much about the rest. Some amount of rainy day fund is always better than no amount of rainy day fund.

Comments

Join the conversation

I already have figure it all out, but it’s always nice to read other opinions. It certainly is helpful!