What Are Sinking Funds & Why Do We Need Them?

We are talking about a different kind of account called sinking funds. We usually end up talking about investment accounts and brokerage accounts 401Ks, IRAs, 403B's accounts like that.

On the flip side, we also talk about emergency funds. Outside of these account types, the other account types don't really get talked about that much.

Common accounts

If you think about it, these investment accounts, retirement accounts, and emergency funds are not really the accounts that we should be turning to frequently.

At least we should avoid it when we can because your emergency fund is there for true emergencies. Like if you lose your job and you need to pay your rent or your mortgage so you don't get evicted and have time to look for a new job.

Your IRA, those are important too but unless you're actually retired you're probably not taking money out of these accounts.

There's another account type that we don't really talk about all that often and that is the sinking fund

What is a sinking fund?

A sinking fund is similar to a savings account but with a purpose on its own.

It's generally just a good idea to set a little money aside here and there because having a little cushion will end up helping you out more often than you could ever realize.

With that thought in mind, most of us don't assign a purpose to our savings accounts. Rather it's just there in case we want it or in case we need it. Maybe you have a decent amount sitting in your savings.

Maybe you keep your savings fairly low. Some people use savings just as a backup for their checking accounts to ensure that they're never charged an overdraft fee.

Do you have an upcoming beach vacation? Put the money for this vacation into a sinking fund.

Maybe you have a big anniversary coming up, or maybe Christmas is coming up. Take the money for these events and put it into a sinking fund.

Really, anything can go into a sinking fund. It's there for those occasional occurrences that tend to show up on a fairly regular basis in our life. That way, when that day it arrives, that money is there and it's waiting for you.

About 74% of Americans have gone into debt to pay for a vacation, according to a new study from the financial planning company LearnVest. 55% of Americans forget to even consider their vacations when laying out their budget for the year.

36% of Americans took on debt in order to pay for holiday gifts this past December.

Without preparing for these events ahead of time, many people end up resorting to debt to take care of them.

That’s a bad cycle to get started when you know you have expenses coming up for these one-time irregular events that, let's face it, happen more frequently than we'd all like to admit.

Having a well-stocked sinking fund or several sinking funds can help you to take these expenses in stride.

Irregular expenses can really throw a wrench in your financial plans. Quite frankly, this is the most difficult part of budgeting. You have those expenses that are the same from month to month, like your rent or your mortgage.

Your groceries are probably pretty similar, utilities are probably similar, and IRA contributions are probably the same from month to month. It's those irregular things that pop up those one-time events or those occasional occurrences that are really hard to plan around.

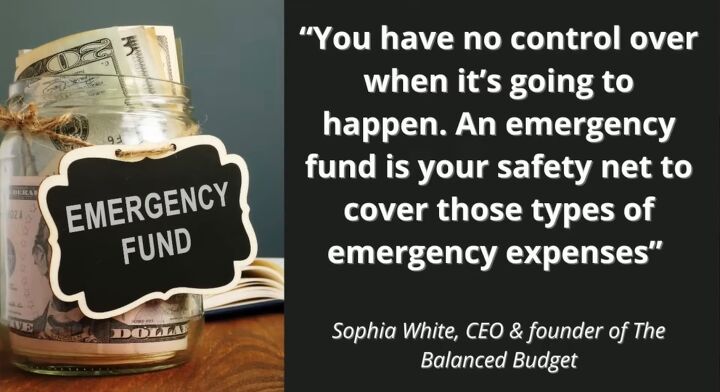

Emergency funds

Now, there is a very big distinction between a sinking fund and an emergency fund. Your emergency fund is there for true emergencies like you or your spouse losing your job. Now, the household has no income. You have no way to make ends meet without this emergency fund. That's when you rely on it.

Or perhaps there's a family emergency that forces you to step away from your job. Again, there's no income. You turn to your emergency fund. It is not just to dip into willy-nilly. There is no concert, no couch, no gift, and no dinner. That is an emergency. You do not touch your emergency fund for those reasons.

You have no control over when it's going to happen.

An emergency fund is your safety net to cover those types of emergency expenses. Most emergencies are unforeseen.

Sinking funds prepare you for expenses that you know are coming up, like an upcoming tax bill or a weekend getaway. Events and items that have a definitive time horizon.

You don't want to go diving into your emergency fund whenever your budget is running just a little bit tight. Your emergency fund is your fund of last resort. It is there, and you want it to be fully funded in case the unthinkable ever happens.

If you've never heard of a sinking fund before or you've never had one before, perhaps it's worth looking into. It can really help to remove some of the stress associated with finances, and it can really put the ball in your court.

Once you know you have an expense coming up, you can start putting money away for it. Once that event or the item arises and that day is there, you have to pay for it. You already have the money earmarked for it, so it's ready to go. You don't have to wonder how you're going to pay for it, and you don't have to resort to debt.

How to start a sinking fund

As far as how to start a sinking fund, sit down and look over your upcoming expenses, paying special attention to those expenses that don't pop up all that often. A vacation, an anniversary, a holiday, things like that. Figure out how long you have to prepare for it.

Create a line item in your budget, and every single week or every single month, have a designated amount go into that fund. So when that day arises, you have the money and you're ready to go.

Sinking funds

What do you think about sinking funds? Have you used them before? Will you use them in the future? Share your thoughts in the comments down below.

Comments

Join the conversation

Interesting article, I have an account that I call Rainy Day. It's separate from emergency and regular savings. I was doing well for first 8 years of retirement, then Covid and Bidenflation took their toll. What do you suggest for people who are tapped out, disabled and can't find a job???

Very good advise.

We have two emergency funds that luckily we did not have to use often. Even thou we had cash around the house, one year our area lost power for about a week, so one of the envelopes is in the event we cannot access a bank ATM.

As a third fund, my husband also saves his coins and dollar bills that we cash in early December to ease our Christmas list.