How to Coast F.I.R.E. - Financial Independence Retire Early

If you’re interested in financial independence and retiring early, this article is a great place to start. When I first started getting into finance, I was very young, and my goal was to save enough money to do whatever I wanted.

I was watching my mom tied to a job that she didn't particularly like, but she needed the paycheck to support her family. I never wanted to be in that position.

I went to school for finance and learned there are a number of different ways to reach financial independence. Most types of financial independence fall under the f.i.r.e. acronym; financial independence, retire early.

There is also lean f.i.r.e., fat f.i.r.e., slow f.i.r.e., coast f.i.r.e., barista f.i.r.e., flamingo f.i.r.e. and more. Each type has the same end goal to save enough that you no longer are reliant on a job or a paycheck. They all have different routes to get there, and that's where the distinctions come in.

Today we're going to be talking about coast f.i.r.e. You save money at a very young age and are able to stop making contributions to your savings. You still reach financial independence sometime down the road, even though you have stopped contributing to your investment. The money continues to grow via compound interest.

You reach this point where you've built enough of a nest egg that you can have a hands-off approach and allow time to work its magic on your money.

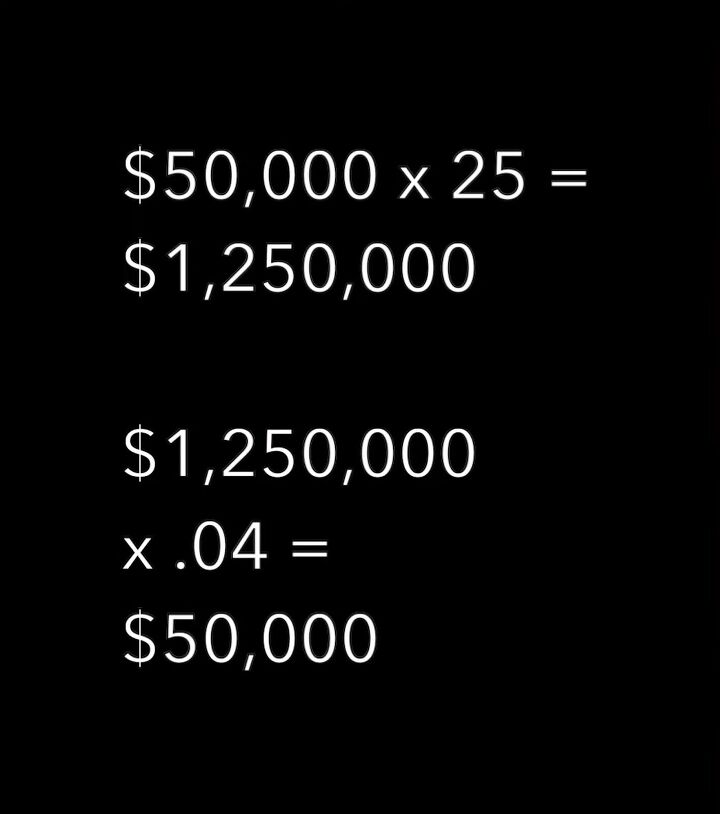

Start by figuring out how much of an annual income you would want to live off in retirement and work backward from there. Say you need an income of $50,000 in retirement. You would need a nest egg of $1.25 million to be financially independent.

We got to that number by taking 50,000 and multiplying it by 25. The rule is you should have 25 times your income to be independent. We can also check our map using the rule of 4%. The Rule of 4% says you can withdraw 4% of your portfolio safely and not risk running out of money in retirement. $1,250,000 multiplied by 0.4 gives us $50,000.

Next, you must figure out how long you need to save and how much you need to save in order to stop making contributions. Say you want to be absolutely done saving by the age of 30. You're going to save aggressively until 30 and then be done.

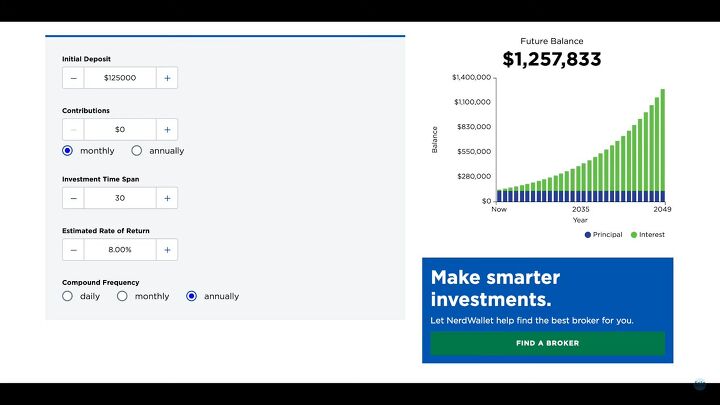

Assuming you want to retire at 60 years old with $1.25 million for an annual income of $50,000, how much would you need to save up? The answer is $125,000.

If you let compound interest take over, assuming an 8% return for the next 30 years, you would grow your money to $1,250,000. That means for the next 30 years, you don't have to save anything at all. Saving up $125,000 by the time you're 30 is no small feat, but that early sacrifice could be totally worth it.

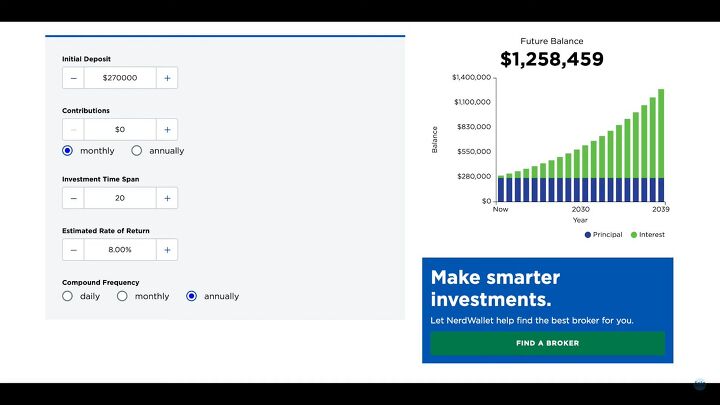

Say instead of being done at 30, you want to save until you're 40, but you still want to reach 1.25 million at 60. How much of a difference is that going to make? If you save until you're 40, you're going to have to save $270,000.

That's significantly more than the amount you needed at 30 because we lost ten years of compounding interest. You have ten more years of savings, but they're going to have to be ten years of aggressive savings.

If you are able to save $270,000 by your 30th birthday, that means you can reach your goals ten years sooner. By the time your 50th birthday rolls around, you would have $1.25 million and you would be financially independent.

There's no one way to do it. The numbers I'm using here are completely arbitrary. I'm just using them as an example. Use the numbers that are meaningful to you.

This approach can be appealing to many who are interested in financial independence because it doesn't require that lifetime of frugality. Coast f.i.r.e. takes advantage of having a significant amount of lump sum saved up and a long-time horizon.

Having a long-time horizon in the stock market is what allows compound interest to do its magic.

Once you have that lump sum saved up, you're essentially financially independent. Left to its own devices, that money will grow to the lump sum you need.

You no longer need to put anything towards investments so you could significantly increase your standard of living. You get to spend your entire paycheck if you want.

There are also some big drawbacks or obstacles that you do have to consider. Number one, you're going to have to be making significantly more than you're spending or it’s pretty much impossible. You must be making enough to put away a large percentage to get that lump sum built up. If you're spending all your income, it's impossible.

Number two, you're going to have to be willing to drastically live below your means. It requires a lot of sacrifices early on. Number three, you are going to need very little or no debt, and or, a very high income.

If you have a lot of debt it's going to be hard to save a high percentage of your income. Being that the average 30-year-old in America has a net worth of about $7,000. It is pretty clear that coast f.i.r.e. is not a relevant strategy for most.

Saving a large sum of money at a very early age is not easy, but it is not impossible. It's easier to save and be frugal when you're younger than when you're older. When you’re young you don’t have anyone else to support or a mortgage to pay.

Financial independence retire early

If you can save a large chunk of money at a young age, coast fire could work for you. I love the freedom it gives you after just a few years of frugality and sacrifice. Leave me a comment and let me know what you think about this saving method.

Comments

Join the conversation

I think this is awesome, however as a woman of color (hispanic) we were never taught these things and now I am 38 with no savings and suffering. Id love some advice/guidance and this point in time of my life. I have 7K in 401 so far, has 14 but took out money to clear my debt (minus school loans which begin again very soon). Any help would go a long way. Thank you!

Where are you getting 8% interest??