How to Start Managing Your Money

This is a sponsored post for PSECU, a not-for-profit credit union. All opinions are my own.

Managing your money is a necessary life skill and really should be taught in schools right alongside math and English. Usually, we make mistakes in our 20s and learn our lessons the hard way. We get into auto loan debt, student loan debt and credit card debt, then are left wondering how the heck we’re going to pay all this off.

If you’re just starting out with learning to manage your money, or if you’re knee-deep in debt and are trying to dig yourself out of a seemingly endless hole, this post is for you. Here is how to start managing your money in an easy-to-understand, step-by-step format.

How to Start Managing Your Money

Take a look at the infographic from PSECU below, followed by my own thoughts on the actions you should take to manage your money.

Step 1: Look at your spending habits

This is the part we all hate, but you do have to take a serious look at your spending habits if you’re serious about getting your finances under control.

What can you cut out? What can you reduce? There are lots of little ways to save money in your day-to-day life, including cutting cable, keeping your thermostat at a reasonable temperature, and only drinking water. If you go out to eat, split a meal with someone or order an appetizer as your meal.

Write down all of your fixed expenses and all of your variable ones, and again, look for ways to cut back. Note how much money you have coming in each month to see exactly what you have to work with.

Tip: If you don’t want to cut back on spending, you need to earn more money. Here are five ways to make an extra $500 each month.

Step 2: Come up with a plan

What are your goals? You might be trying to get out of debt, save for a down payment on a house, or live off of just your spouse’s income within the next year. Whatever your goal is, you need to have a plan in place.

Write down your long-term goal, followed by your “mini goals” that will help you get there. Then, make a list of daily and monthly goals that align with your long-term goal to keep you on track.

If you want to eventually be a stay-at-home mom, for example, here’s what your plan might look like:

Long-term goal: Live off of one income

Mini goals: Pay off all credit card debt, save $12,000 within one year

Monthly goals: Save $1,000/month (this could be the working mom’s earnings, or you could side hustle to make more money), put $300 towards credit card debt

Daily goals: Create meal plans, avoid going out to eat, avoid coffee runs, etc.

Step 3: Pay debt and build savings

This aligns with Step #2 in coming up with a plan. Regardless of your end goal, you should be focused on paying off debt and building savings. Paying off debt gives you freedom to quit your job, work part-time, change careers, spend more time with your kids, and more.

Savings is extremely important in the event of an emergency, such as a job loss or an unexpected expense. Did you know that only 15% of Americans have $10,000 or more stashed away? If you or your spouse lost a job suddenly, what would you do? Having money set aside for living expenses (six months is ideal) is vital. Not only will it give you peace of mind, but it will allow you to live a bit more comfortably and sustain your lifestyle if something happened.

Step 4: Look at your monthly spending, again

Is that gym membership going unused? What about those magazine subscriptions? Did you pay any late fees or overdraft fees? All of these seemingly little expenses add up quick. Take a really close look at your spending each month and see what all you’ve missed.

Another tip from PSECU is to pay all of your bills online so you avoid the cost of stamps. $0.49 might not seem like much, but over the year it can add up to over $200 if you pay all of your bills by mail! What would you do with an extra $200?

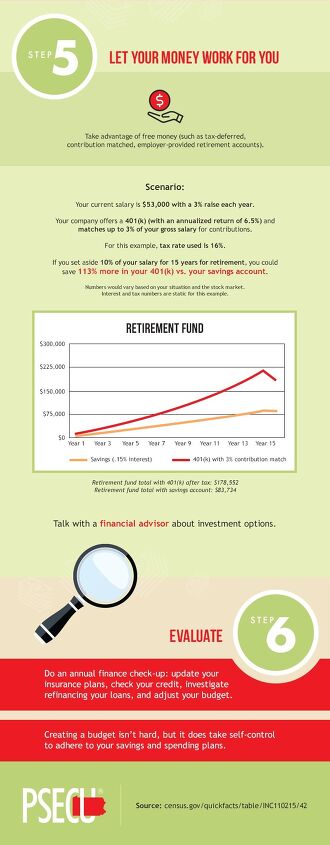

Step 5: Start investing

Once you’ve paid off your debt and built up a savings account, it’s time to start letting your money work for you. In other words, start investing!

A great place to start is your company’s 401K account, assuming they offer one. The PSECU infographic shows if you set aside 10% of your income (assuming $53k/year) for 15 years, you would have 113% more in your retirement versus a regular savings account alone! Compounding interest is a beautiful thing.

Step 6: Review, update, repeat

Even when you have no debt, money in savings and are investing, your finances can never be on autopilot. It’s always a good idea to check in at least once a week and make sure your budget is on track.

A final tip…

We haven’t had to be on a serious budget in almost four years. We have no debt outside of our mortgage and have a decent amount of money in savings. I’m a SAHM/blogger and my husband is the main provider financially. Me taking on side jobs and starting a blog is what allowed us to have freedom from 9-5 employment (my husband works for himself, too!) and to follow a looser budget!

If you’re interested in blogging or freelance writing, here is my tutorial to get your website up and running. Blogging will not earn you money right away, but if you’re consistent with it and have a good business plan in place, you WILL see results!

What is your best advice for managing your money?

Comments

Join the conversation