How to Start a Zero-Based Budget in 10 Easy Steps

Today I’ll introduce you to zero-based budgeting! A zero-based budget means you give every dollar you earn a job so you can make sure you’re doing the very best with what you have. I've loved different budget methods but this budget by far gives the most accountability, in my opinion.

1. Create a sheet

(Note that this budget does not consider life insurance or health insurance costs. I’m making the assumption that your life and health insurance premiums are probably taken out through your employer or you receive it through the government. In other words, everyone’s situation is different.)

We are going to create a fictional budget but don’t get too hung up on numbers.

When you’re trying to create a zero-based budget, you’re basically giving every single dollar you make or that enters your bank account a real job.

There’s no free money or extra spending money floating around in this type of budget. This is to make sure that all of your money is being accounted for.

2. Know what income you have

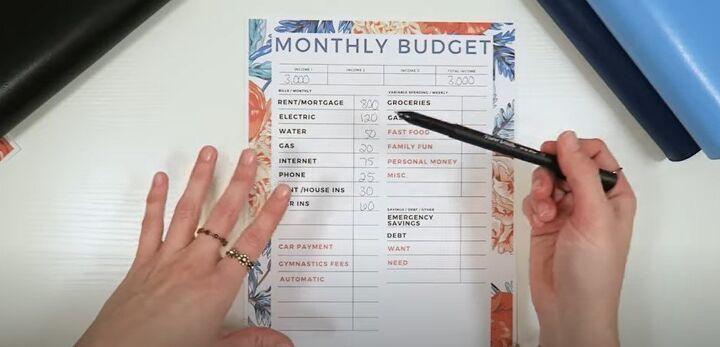

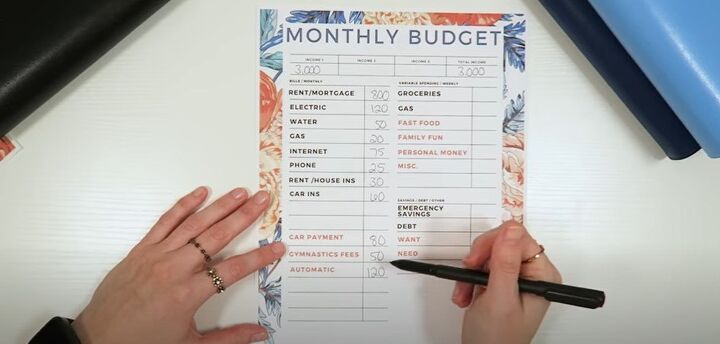

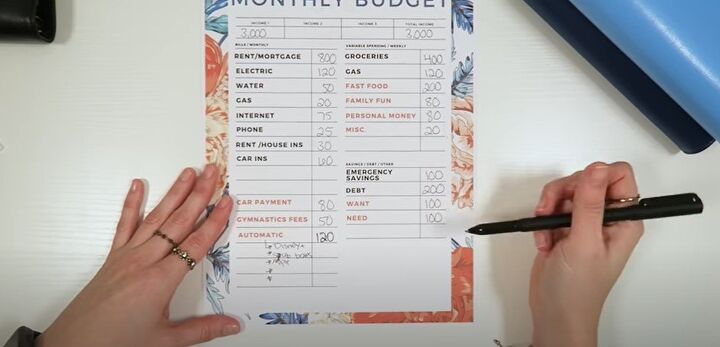

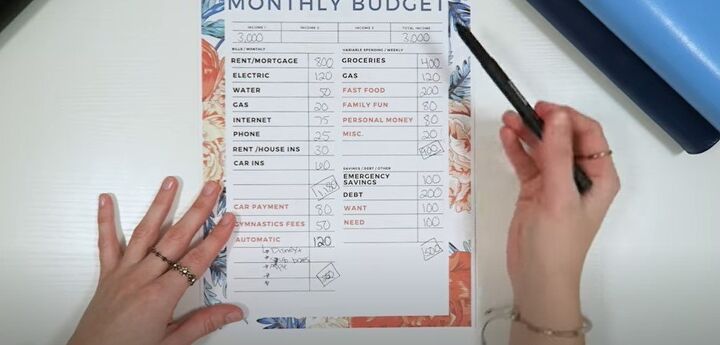

We are going to assume for the purposes of this fictional budget that there’s a $3,000 a month income and our rent or mortgage is $800. Everyone’s expenses and numbers will differ.

Here’s $3,000 coming into our bank account. Let’s assume we don’t have a second or third income, so the total income is $3,000.

3. Enter monthly bills and expenses

Let’s fill in the monthly bill section and assume we spend the following every month:

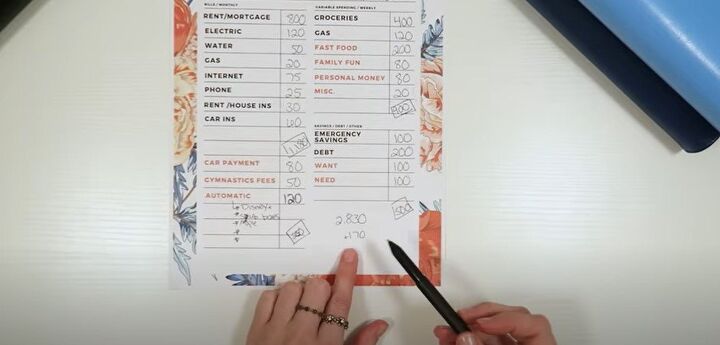

- Rent/mortgage–$800

- Electric–$120

- Water–$50

- Gas–$20

- Internet–$75

- Phone–$25

- Rental insurance–$30

- Car insurance–$60

- Car payment–$80

- Gymnastics class fee–$50

- Misc. automatic purchases–$120

You may have a couple of other categories so you can fill in the blanks.

4. Tally automatic purchases

To get the miscellaneous automatic purchases number, go through your credit cards and debit accounts to find all the automatic payments like streaming services, subscription boxes, Apple fees for products.

List them all out and cancel any of the purchases that you don’t need anymore. I think in today’s world this is where a lot of us waste a lot of money.

5. Enter variable or weekly spending

You’ll notice on my sheet there are different colors for some items. But in this column, we have:

- Groceries–$400 or $100 a week

- Gas–$120 a month

- Fast food–$200 a month or $50 a week

- Family fun–$80 a month or $20 a week

- Personal money–$80 a month or $20 a week if things pop up

- Misc. –$20 a month

You can do away with the miscellaneous line if you don’t like that “free” money hanging out there by itself. But it’s always nice to find $5 extra dollars so I keep that line in my budget. It’s just my tiny wiggle room.

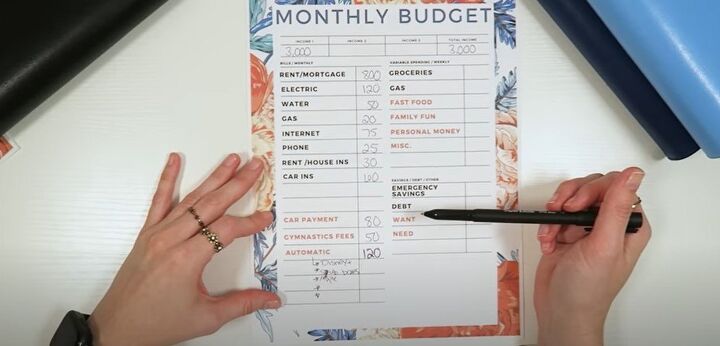

6. Enter savings

- Emergency savings–$100

- Debt–$200

- Want (savings)–$100

- Need (savings)–$100

7. Add it all up!

I have my calculator ready to total it up.

- The bills section totals $1,180 per month.

- The lower payments section (car payment and automatic payments) totals $250 per month.

- Our weekly expenses totals $900 per month.

- Our savings, debt, and other, we are putting away about $500 a month.

With our $3,000 hitting our bank account every month, and with all the spending and savings we accounted for, that puts us at $2,830. We have $170 left over after we have paid all of our bills, expenses, and put money into where we need it to go.

8. Account for extra money

In a zero-based budget, we don’t let that $170 roam free. It doesn’t become shopping money or buffer money in our account. We would decide what that $170 needs to go towards and give it that job.

I would recommend putting it towards the consumer debt to get it knocked out sooner. So, I’ll have $370 going directly toward debt this month.

You will then need to track your money all month to see how realistic the budget you put on paper works for you. You’ll need to make adjustments, most likely.

9. What if you spend more than you take home?

If you find that you make $3,000 a month but you’re spending $4,000 a month, you need to take a look at some categories. Or, create a second or third income.

Your rent/mortgage and that column is not necessarily fixed, but hard to reduce. I would look to reduce the following categories:

- Car payment–try selling the car and getting a cheaper one to reduce payments

- Automatic payments–you may need to substantially narrow down this category.

- Activities for kids–you may need to cancel these temporarily.

Don’t stop paying off debt and don’t stop saving but I may reduce what I put into the “want” and “need” savings accounts.

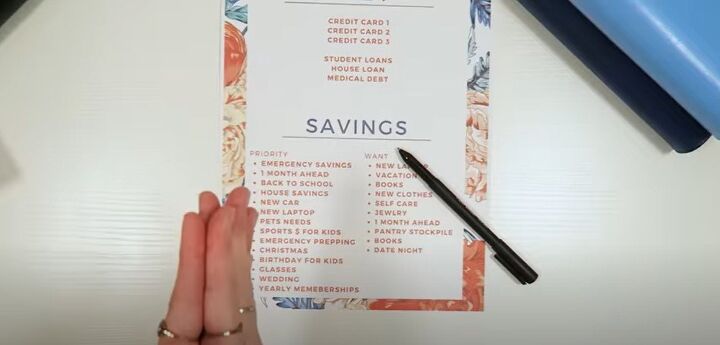

10. Let’s talk about savings and debt

Consumer debt should be the first priority to eliminate. Next, pay off student, housing, and medical debts. They are a high priority, but not as big of a rush as consumer debt.

Savings can be broken down into so many categories of priorities, needs, and wants. For example, you may have priorities such as emergency savings, Christmas, back-to-school shopping, or you need a new car. These categories can be stressful if you didn’t start saving up ahead of time.

A “wants” list would be a vacation, new clothes, jewelry, and things like that.

How to start a zero-based budget

This zero-based budgeting template is a starting point. I hope learning what a zero-based budget is all about inspired you to take more control of your finances. Let me know if this is the kind of budgeting you can comfortably live with.

Comments

Join the conversation

How much do you put aside for 1-month ahead?

I am not computer saavy, so a copy of your template would be so helpful.