Should I Pay Off Debt or Invest? Here Are 7 Things to Think About

A very common question I see come up a lot is, should I pay off debt or invest? The advice and the response I see that comes up a lot online, again, is very black and white and I just don't think personally that is so simple. I developed a checklist to help me answer that very question for myself when I was looking to invest.

1. Are you over 35?

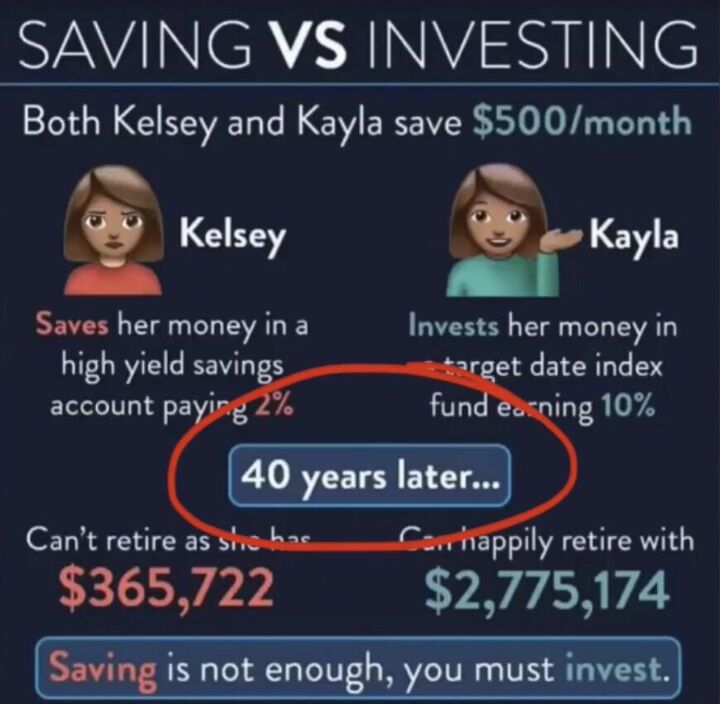

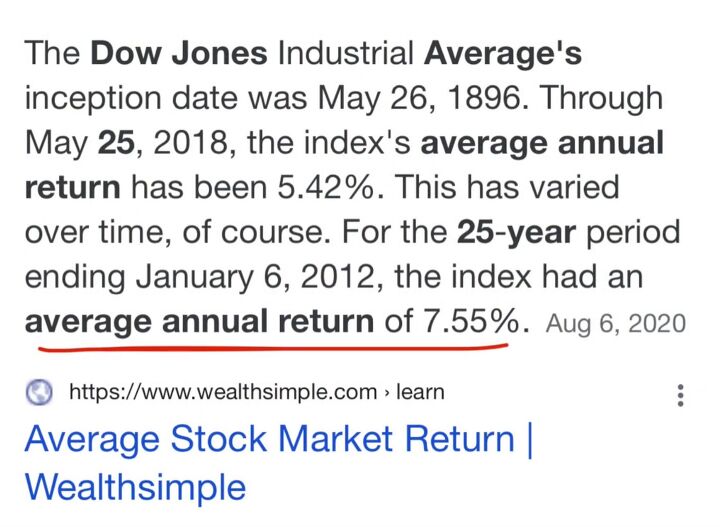

Are you over 35? I think this is a critical age because over 35, your timeline is shortened. Most advice I see online about investing says, with 40 years of $100 towards whatever IRA, you'll be a millionaire.

Well, once you get over 35, the timeline of 40 years starts to not apply anymore. We're looking more like 25 or 30 years. Our timeline is just shortened.

When you have such a long time to invest, especially in stocks, stocks are a little riskier, but their reward is higher, meaning the return that they can earn is much greater than bonds or just cash reserves like a savings account.

So when the market is doing this up and down thing, as it always does, when you have 40 years to invest, the volatility just doesn't have the same sort of impact on a 25-year-old as it might a 45-year-old.

2. Does your company offer a 401K with a match?

Now, matches are an incredible thing to have and I especially love them for people who cannot put a significant amount of money into an investment.

If they're able to invest at least $50 a month, $25, whatever it is if the company matches one-for-one, they'll likely be given that exact amount from the company as well. So if you put in 25, they put in 25, and you can double your investment power simply by taking advantage of a match.

3. Do you have a fully-funded emergency fund?

An emergency fund is the fun you should go to if you have major emergencies like job loss or health issues. A lot of people who are getting to the place of getting their emergency fund in order will lean on credit cards.

That's not what we want to do. We don't want to dig ourselves into a bigger hole.

So to invest, I think it's important to have at least three months' worth of living expenses saved so that you have that to lean on before diverting money into investments, which I think are secondary to emergency funds.

4. Are the interest rates on your debt at 7% or lower?

This is another key marker for me because at this point, if you have debt with 7% interest rates or lower, theoretically you could be earning more money in the market than you are by paying that money out in debt.

So that's not to say that you should just stop paying on that debt once you get to a 7% interest rate or lower on those items. It just means that now instead of putting all $200 that you earned in your side hustle on debt, maybe you put $150 towards debt, and then $50 of that $200 goes to investments.

5. You don't feel comfortable missing more than two years of investing

If you're able to answer yes to that question, then this is another indicator that you might be ready to start investing.

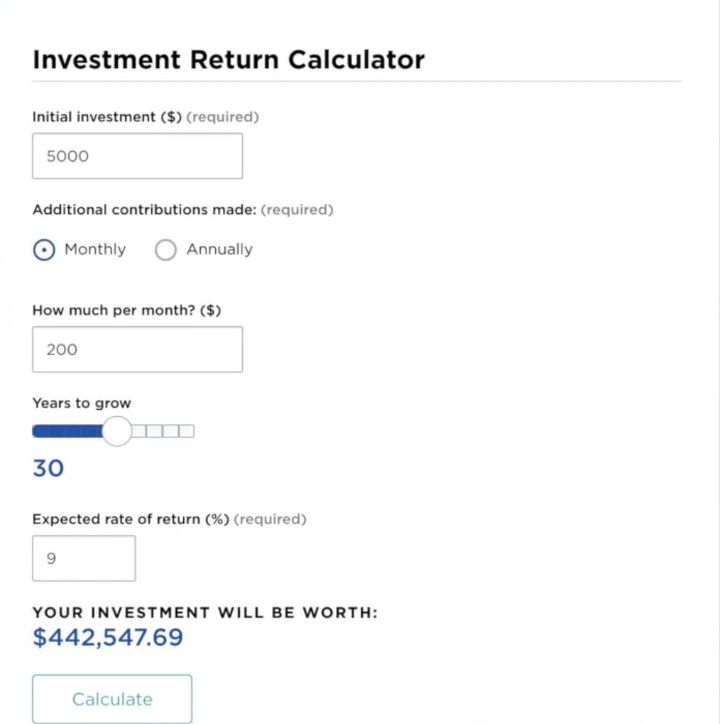

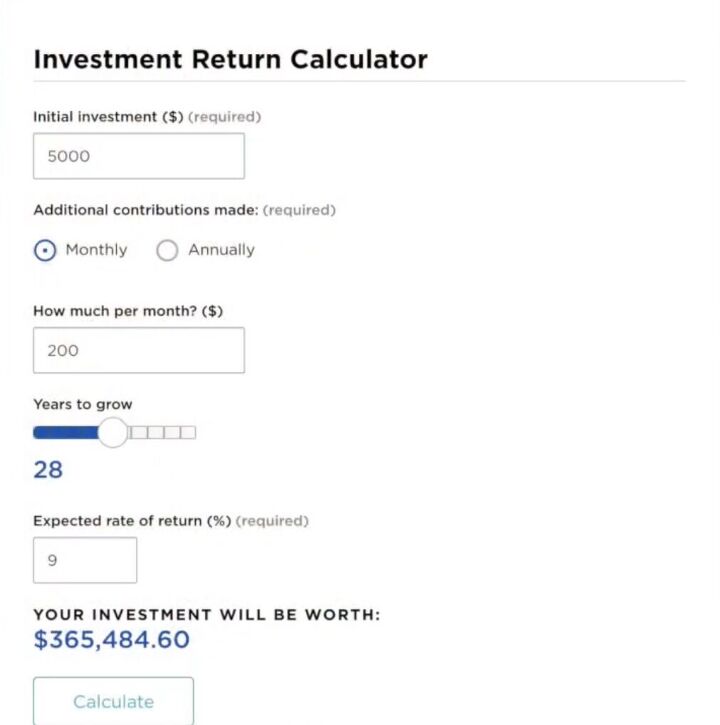

There are tons of calculators online that will show you all about how to theoretically calculate your return on interest. If you put in 30 years as a projection in that calculator for what you're investing and you get a number, maybe you're okay with that number, what that looks like in 30 years.

Then you change it to 28 years. That means you will miss two years of investing. Once you put in 28 years, whatever that number that gets spit out from the calculator says, if that number makes you think you prefer the 30 years to the 28, then I don't think sitting on the sidelines more than two years is going to be a benefit for you.

6. Paying off my debt is important to me, but it doesn't keep me up at night

Again, if you can say yes to that particular statement, you might be in a good place. If you are in a position where you have debt and it is keeping you up at night, meaning it's disturbing to your health, and your mental health, then probably getting that debt paid off as quickly as possible will be the priority for you.

If you feel like you're in a good place and you're like, okay, I got debt, but it's not like crushing me and I'm able to live a pretty decent quality of life while still managing my debt, then investing might be an okay way for you.

7. I have a solid debt repayment plan and I feel in control of my finances

So this one is very much like the last one and it's getting to the underlying health and quality of life factors that go into money and the emotions around it.

If you feel in control of your finances and you know you have debt and you know you need to save and invest, but you're okay with where you are and you feel like you're making good progress, then I don't think it's so bad to divert a little bit of money to invest.

Should you pay off debt or invest?

I think that list that I came up with tackles all the different areas that we need to consider before deciding to invest.

I hope my checklist has been able to help you to decide whether to invest or pay off debt, or even a bit of both. You have options, so choose what works best for you and your budget.

Have you started investing? If you have, what did you start investing with? Share in the comments, we love to hear from you!

Comments

Join the conversation