How to Stop Overpaying Tax & What to Do With a Tax Refund

It's officially tax season, so I want to show you how to save money on taxes. Maybe you're in the middle of filing your taxes, or perhaps you're an early bird who's already taken care of everything. About 75% of tax filers get a tax refund every year, which averages $3,000 to $5,000.

Tax refunds

A tax refund is your hard-earned money being returned to you, money that you overpaid in taxes.

So if you're one of the millions getting a tax refund, as most tax filers do, you gave the government a loan for the low rate of 0%.

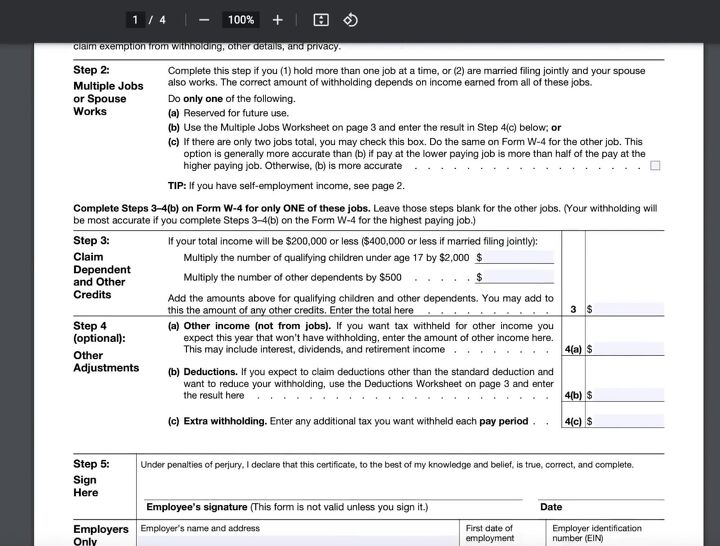

Adjust your withholding

If you routinely get a large tax refund, all you have to do is fill out a new W-4 form, adjust your withholdings, and then give that form right back to your employer. That will give you more money to work with throughout the year rather than waiting for a one-time tax refund.

With over 100 million people gearing up to receive a tax refund, I thought it might be a good idea to go over some of the best ways to maximize this refund to set yourself up for financial success.

Pay off high-interest debt

If you have any high-interest debt, like an outstanding balance on a credit card sitting at a high-interest rate, take that entire tax refund and send it along to pay down this debt or completely wipe it out.

Making any headway with your finances is nearly impossible when compounding interest is working against you at 20%.

Then remember, while credit cards are a great tool, if you can't pay off that balance in full every month, you have no business having a credit card.

Set up an emergency fund

Having a well-funded emergency fund is a cornerstone of a sound financial plan. If you don't have an emergency fund, you're vulnerable to whatever life throws at you.

If your emergency fund is running low and you're anticipating a tax refund, now is the time to build it up.

An ideal emergency fund would be anywhere from three to six months' worth of expenses, potentially more if you're retired, a single-income household, or a freelancer with an unpredictable work schedule. It might be closer to eight months or a year in that situation. Ideally, you will keep your emergency fund in readily accessible cash-like accounts.

Of course, that's not to say you shouldn't be earning any interest on your cash or emergency funds. I want you to take advantage of high-yield savings accounts, CDs, or T bills. You want to make sure that this cash is there when you need it, and in the meantime, you want to be paid a decent interest rate.

Retirement savings

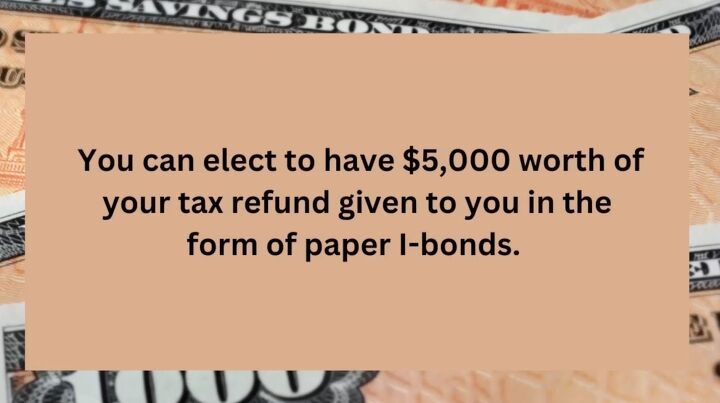

If your tax refund is larger than $5,000, and after investing in I-bills, you can elect to have the remaining amount deposited into an account of your choosing.

One thing about retirement accounts, specifically the Roth IRA, is that they could double as your emergency fund in a pinch.

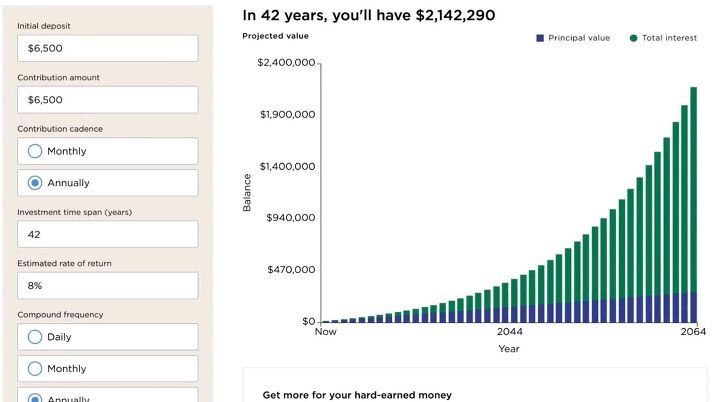

However, your Roth is better utilized as a retirement account, allowing your money to grow completely tax-free until, one day, you can make your withdrawals completely tax-free. Let compounding work its magic when you can.

Roth IRA

Let's say you have no debt and you already have an emergency fund in good shape. The next step would be to put this money to work, and a great option is the Roth IRA.

A lot of the benefits of the Roth IRA were already mentioned, and this money gets to grow completely tax-free until you reach retirement age 59 and a half, then you can start making withdrawals completely tax-free.

If you haven't maxed out your Roth from 2022, you can still do that until tax day. If you've already maxed out your Roth from 2022 and you're ready to get started on your contributions for 2023, this is a great position to be in. That means you're getting started on funding your accounts early in the year.

Pay down your mortgage

So what if you don't have any credit card debt, and you've already got a flush emergency fund, and your retirement or your IRA box is already checked? I'll throw out some ideas, but you have a lot of freedom here.

Perhaps consider paying down your mortgage, baby-stepping towards paying it off. We all feel differently about mortgage debt. For some people, the goal is to be completely debt free. If that is your goal, this can be a step that helps you get there sooner.

Tackle a home renovation

Is there an area of your home that needs some sprucing up? Maybe it needs to be repainted? A little bit of a facelift? Maybe some repairs need to be made? Maybe you need some new appliances. This tax refund can help get you started there. This can help to increase the value of your home.

Invest in a 529

You can invest for your kids or grandkids by putting this money into a 529 to help with future education costs. If you don't want to use it as an education fund, maybe use this money as a learning opportunity to help teach your kids about investing and get them excited about it.

If your kids are working age, you can help them set up their own Roth IRA account and tell them you'll match any contributions they make to that fund. You can use your tax refund or your bonus money for this purpose.

Have fun

If all of your bases are covered, live it up. Plan a vacation with your significant other. Maybe splurge on something you've been holding back on. Once all your necessities are covered, it's time to have a little fun.

What to do with a tax refund

Also, remember to check your W-4 so you don't get a refund next year. Are you getting a refund? What are your plans for it if you are? Leave your ideas in a comment down below.

Comments

Join the conversation